Intuit deep dive

A PDF version of this Intuit deep dive is available to premium readers at the end of the report.

I have an investment proposal for the next 30 years. During the holding period, here’s what I guarantee will happen:

Its flagship product will become irrelevant within a decade

Operating profits will decline for the first five years

Microsoft will spend the next decade attacking its main products

It will face a leadership crisis once its founder steps back

Three technology shifts (internet, mobile and AI) will challenge its competitive advantage

Lastly, you can expect at least three 50% share price drawdowns during the holding period

Most rational and risk-conscious investors would likely pass.

Despite these challenges over the past three decades, Intuit’s shares delivered a 42-fold return, or 13.4% annualised return, quadrupling the S&P 500’s return (11-fold or 8.4% annualised return) during the same period.

Like previous technological shifts over the past three decades, there’s once again doubt and worry about the future of the five foundational software companies (Adobe, Intuit, SAP, Oracle and Microsoft)

Market capitalisation (As of 21st May 2026): $84.9 billion

Jenga IP 2030 FY estimated market cap: $161.9 billion

Potential IRR (including dividends and buybacks): 20.3%

Jenga IP Quality Rating: 76.7/100

“Quicken [Intuit] is over! … It’s done. It’s almost a non-factor. Intuit is learning the hard way that owning a market niche doesn’t mean much when new technology comes along and washes it all away” - David Farina, August 1997, Fortune issue.

Among the five companies, Intuit arguably had the most fragile-looking path and now faces existential AI-era questions. Its investment case now sits on five questions:

Can Intuit maintain its ecosystem control of financial services to American SMBs?

Can Intuit reduce churn across its payroll and payment solutions to SMBs?

Does TurboTax become a higher moat business as it transitions from DIY to expert assisted?

Does AI serve as a net positive or negative for Intuit’s competitive advantages?

How lucrative do OpenAI and Anthropic perceive the bookkeeping and tax preparation market?

To answer these core questions, here’s what I’ll cover in the Intuit deep dive:

Table of contents

Intuit’s history: Insights into Intuit’s transition from personal finance (Quicken) to a multi-product SMB and consumer ecosystem, efforts in scaling SMB and consumer software solutions across the decades, case studies on product challenges and pivots, culture and capital allocation, and the durability and weaknesses of its competitive advantages.

SMB financial services industry: An overview and analysis of Intuit’s SMB financial services markets, ranging from accounting software to payroll and payments. A comparison between Intuit’s QuickBooks and key competitors (Xero, Sage, Block and Paychex). The customer’s view across the U.S. and international markets.

The tax preparation industry: The legal, historical and competitive architecture of U.S. tax filing, TurboTax’s market position, assisted versus digital shifts, IRS Direct File and the long-term durability.

Intuit’s product suite: An assessment of Intuit’s product scope (QuickBooks, Mailchimp, TurboTax and Credit Karma), product plans and pricing, product architecture on a usage and per seat monetisation and usage versus per seat economics and product innovation.

Intuit’s AI opportunity and challenges: A deep dive into Intuit’s AI efforts, customer feedback and traction, an overview of AI-native challengers targeting Intuit’s solutions and an analysis of solutions at risk from AI.

Intuit’s business economics: Analysis of Intuit’s revenue and costs by segment (Global Business Solutions, Consumer, Credit Karma and ProTax, economic contribution of acquisitions such as Mailchimp, broader assessment of Intuit’s competitiveness and a unit economics analysis of QuickBooks and TurboTax.

Growth opportunity: Analysis of its growth drivers via ARPU expansion, customer growth and insights into its potential product expansion, a review of past international growth failures and current opportunities.

Risk and challenges: Further assessment of the competitive threat and challenges across AI-native, payroll specialists and vertical software companies, overpricing risks, tax simplification attempts, share-based compensation reliance and the non-GAAP reconciliation, and final thoughts on AI-driven seat compression and ecosystem control.

Valuation: An earnings multiples-led valuation and projection of Intuit’s earnings potential through to 2030 FY, comparison with peers and the broader software industry.

Conclusion: Final thoughts on the software downturn, insights into portfolio management and sizing a potential investment in Intuit.

1. Intuit’s history

Like many software companies, there’s some scepticism about Intuit, a provider of bookkeeping, tax and personal finance solutions, in today’s AI world. Will people file taxes directly on LLMs? Will businesses transition their payroll and accounting directly to chatbots rather than Intuit’s QuickBooks? Or will individuals depend more on AI platforms for personal finance planning than Intuit’s Credit Karma?

To answer these questions, it’s important first to understand where Intuit has come from, why it became the most successful bookkeeping platform globally despite 46 other software companies coming before them, and why larger technology companies like Microsoft failed to beat Intuit in its own game.

To appreciate its business resilience and anti-fragility to date, it’s best to examine its evolution in four phases:

Phase 1 1983 - 2000. The Scott Cook era

Phase 2 2000 - 2008. The Steve Bennett era

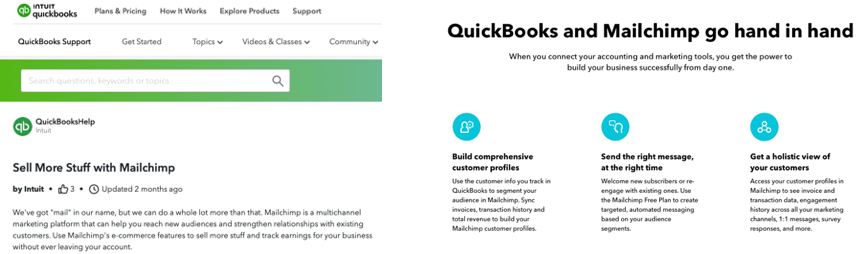

Phase 3 2008 - 2018. The Brad Smith era

Phase 4 2018 - present. The Sasan Goodarzi era

Phase 1 1983 - 2000. The Scott Cook era

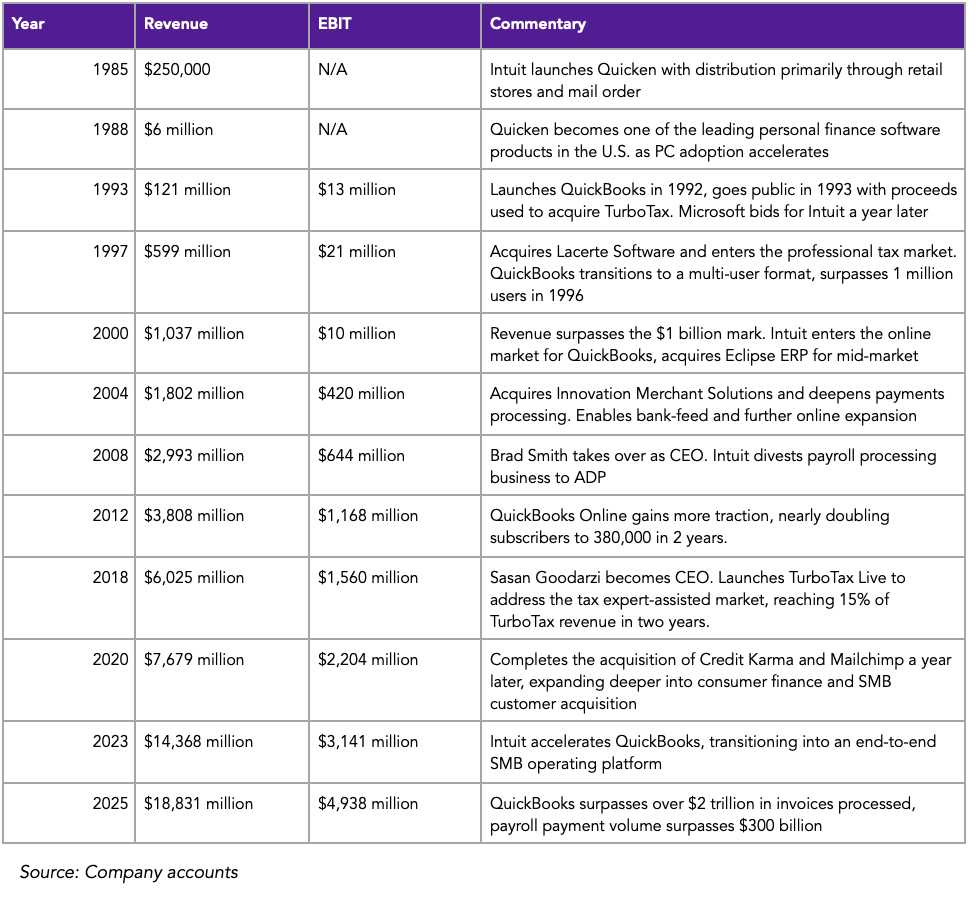

For the first decade, though, Intuit wasn’t in any of these markets. 3 of its 4 core platforms were acquired while QuickBooks grew out of what Intuit was initially known for, Quicken, or as initially called, Kwik-Chek.

Intuit’s founder and current board member, Scott Cook, noticed his wife’s challenges with balancing their family’s checkbook, and he figured he could solve this challenge through personal computers. Although his marketing experience at Procter & Gamble proved valuable in shaping Intuit’s growth strategy over time, to get off the ground, he lacked the required technical software development knowledge, and to fill this gap, Intuit’s co-founder, Tom Proulx, a then student at Stanford University, joined as the programmer and wrote the first version of Quicken.

Although certainly important, Quicken’s success wasn’t simply due to outcompeting peers in technology. There were already 46 players in the personal bookkeeping market prior to Quicken’s entry, and their success was mainly due to four reasons:

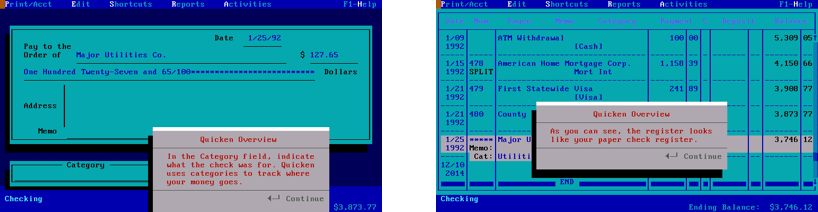

Simplicity: Inspired by Apple’s Lisa user interface, Scott Cook concluded that the best way to approach the personal finance software market, at that time, was ensuring its user interface looked like a real-world checkbook interface. Then market leaders like The Home Accountant and Managing Your Money by MECA had focused too much on features and showcasing their software capabilities rather than actual customer needs.

Financier Personal Series by Financier Inc of Westboro, Mass had even gone as far as enabling 33,000 types of accounts, with its listing price set at $195, more than double Quicken’s price. Quicken, unlike peers, was fully focused on actual customer needs guided by customer research. The philosophy here inspired the company name “Intuit” as the tools needed to be “Intuitive”.

“Manage Your Money by MECA Software of Trumbull, Connecticut, was so complicated that the staff at a software convention MECA booth failed to make it work. “This program is like an adventure game, it’s so hard!” A MECA employee exclaimed to Cook.” Inside Intuit by Suzanne Taylor

Follow Me Home: Scott Cook’s consumer background was particularly helpful for Quicken in winning customers. To ensure the experience left customers “delighted”, Scott Cook instituted a “Follow Me Home” research process where both marketing and engineering staff followed willing first-time customers home from software stores, watching them install and use Quicken.

While closely watching customers, engineers took notes of any feature lags and when customers seemed confused, hesitated or reached for the manual for further explanation. The feedback here, coupled with the internal database order-entry system created by Proulx to track customer comments, ensured that Quicken was optimised for the customer experience and user ease.

Every employee in the company answered customer service and support calls at least four hours each month and also created a customer advisory panel, led by loyal Quicken customers. Today, these seem obvious from a business strategy, but in the wake of the software world in the 1980s, customer obsession wasn’t central to business strategy.

Frugality: A key reason Intuit, alongside other foundational five software companies like Microsoft, SAP and Adobe, survived and thrived for decades was their frugality due to limited funding and operational budgets. Despite being right at the heart of Silicon Valley, Scott Cook only raised $151,000 from friends and family to launch and scale Intuit.

Frugality was necessary for survival and guided every decision at Intuit. For example, to cut COGS by half, Quicken resized the program disk and manual to save on packaging.

After partnering with banks to sell Quicken to customers, management streamlined marketing and advertising to the beginning or end of their fiscal years, saving unnecessary costs. By the fourth quarter of 1985, Intuit became cash flow positive.

Partnerships and distribution: Given the limited budget, Intuit couldn’t initially scale via retail campaigns and stores as aggressively as larger and more established peers did. As alternatives, they focused on working with partners who benefited from Quicken’s rise.

For example, Apple admired Quicken’s interface and ease, and it also increased the use case of Apple’s personal computers. Banks across the U.S also benefited from Quicken because it made customers more engaged with their bank accounts, driving account retention and product purchases. One of the successes here was the Bank of Hawaii, which single-handedly drove Quicken into becoming the top consumer software in the state.

The financial success gained from these partnerships provided Intuit with the resources to then expand through the more traditional software stores, signing deals it couldn’t previously close due to its then small scale. Between 1988 and 1990, sales grew five-fold, from $6 million to $33 million.

You may have also noticed that unlike other foundational five software companies, the product name (Quicken) and company name (Intuit) were different from day one. This is quite important because Intuit has never been about a single product or solution. It’s always been about simplifying financial management for customers, and Quicken was simply a stepping stone for a longer journey.

Always on the hunt for expansion, Intuit began surveying small businesses as early as 1988 to gauge if it could broaden its tools beyond personal finance. It was immediately evident to Cook there was an opportunity among SMBs, and he later hired Sam Klepper to lead the efforts, and after noticing a Quicken Payroll add-on called QuickPay, created by Mike Potter, Intuit doubled down on separating the SMB accounting service, and QuickBooks was launched in April 1992.

Unlike consumers, SMBs couldn’t avoid periodically updating their bookkeeping, making QuickBooks more of a software staple than Quicken’s discretionary use case (another key quality attribute), which led to a more recurring, stickier and more resilient to economic shocks product base. By the second half of the 1990s, it became clear to management that QuickBooks would be more important for Intuit than its original Quicken, and they would later sell Quicken in 2016 to focus on QuickBooks.

Acquisitions also played an important role in growth, although not all of them worked. In 1993, it acquired ChipSoft, owner of TurboTax, further increasing the business stickiness, while bolt-on acquisitions like National Payment Clearinghouse in 1993, Parsons Technology in 1994 for SMB software, GALT Technologies in mutual fund distribution and Lacerte software in 1998, addressing the professional tax software, supported the core Quicken and QuickBooks platforms.

Intuit had also diversified into physical financial supplies like printed checks, deposit slips, tax forms and payroll checks and by FY 1997, they reached 15% of their revenue, growing even faster than pure software sales.

Phase 2 2000 - 2008. The Steve Bennett era

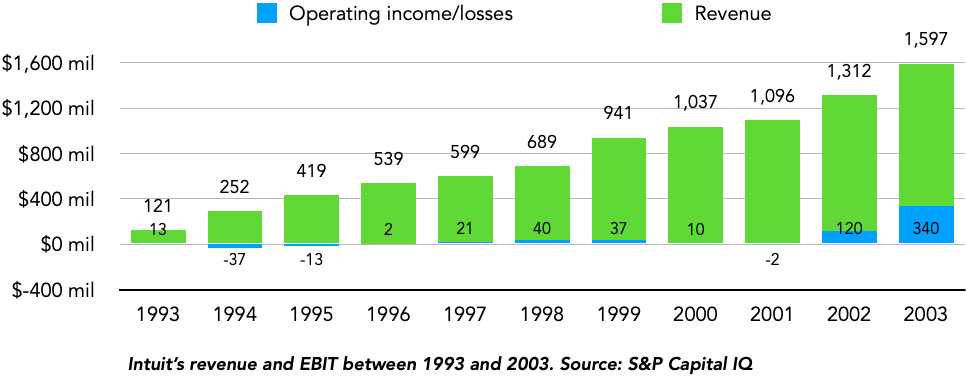

Despite the impressive revenue growth, from $33 million in FY 1990 to $1,037 million by FY 2000, a 41% CAGR and share price return of 645% between its IPO and the end of 2000, Intuit still wasn’t a rock solid company. Markets worried about the health of Quicken given the cyclical and fad nature of personal finance software (more on this when we discuss Credit Karma later on), and between Nov 1995 and April 1997, Intuit’s shares lost 72% of their value as profitability still dwindled. To improve its fortunes, Intuit promoted Bill Harris, who had joined through the ChipSoft acquisition (parent of TurboTax), to lead Intuit’s internet aspirations.

During his tenure, not only did profit margins remain tepid with slowing sales growth, there were culture clashes between Harris’ management style and the Intuit team, leading to his shortly lived CEO tenure. To ensure the board didn’t repeat this mistake, Scott Cook took a more hands-on role in picking the next successor and Steve Bennett was hired from GE in January 2000 to turn around Intuit’s fortunes and refocus the group into productive and profitable segments.

“He [Bill Harris] took the job around August 1 and within a week he was floating around book ideas. He was supposed to be the CEO!” Inside Intuit by Suzanne Taylor

Bennett’s more decisive and bottom-line focus, the Jack Welch way, was required during this period as the tech bubble burst. The increased focus was most evident in the QuickBooks 2003 release, as the bug rate had reduced by 70%, driven by process excellence techniques and defining specific tasks by phases.

“At one meeting, some managers presented a forecast for increasing page views. He said let me understand something: if you get more page views do you get more revenues?… So what drives revenue? So if page views go down you can still get more revenues.

“Steve taught us you can have hundreds of measures but if you’re not measuring the right things or if they’re too hard to measure you can really mess up.”

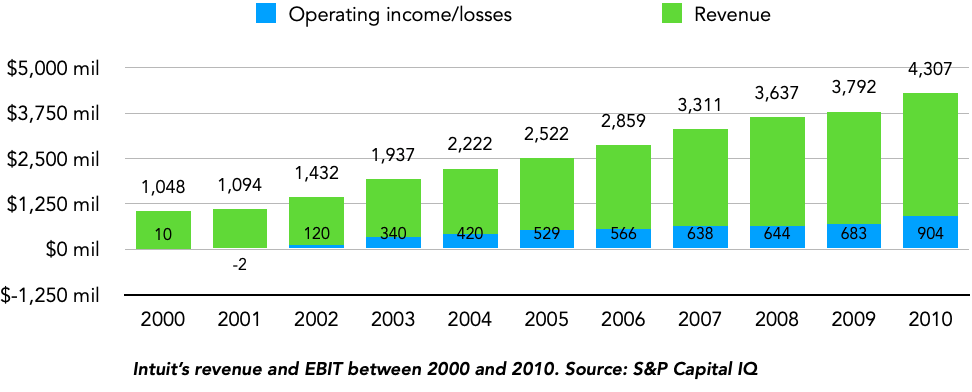

Coupled with improvements in TurboTax, which had reached a market share of 71% by 2003 with over 5 million desktop sales, Intuit’s financial performance greatly improved during its GE era of rightsizing and efficiency, with operating profits growing from $10 million in FY 2000 to $644 million by FY 2008.

Commentators often overlook this era of Intuit due to its share price decline of -7% during this period, but this was really the most important period for Intuit’s journey in transitioning into a financial management operating system.

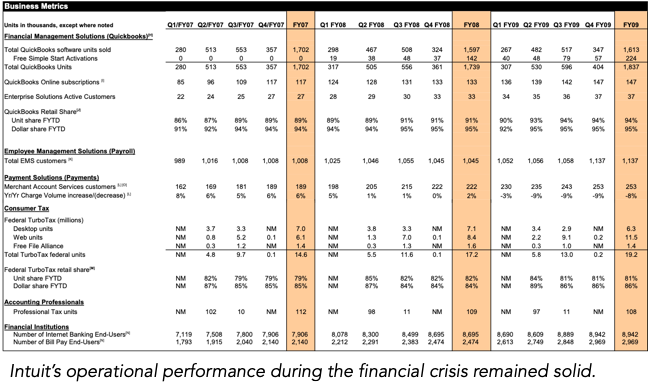

Case study: The Financial Crisis

Although Intuit is very different from where it was during the financial crisis, it’s always useful to examine how companies deal with crises. Another pillar of my quality investment thesis for Intuit is its ability to withstand challenges.

Crisis or not, individuals still need to file taxes (+7% FY 2009 growth), while businesses still demand bookkeeping (-2% FY 2009 growth), file payrolls (+8% FY 2009 growth), and make payments (+14% FY 2009 growth). On the other hand, personal finance, being more discretionary, often experiences less user demand, and its revenue fell by 14% in FY 2009.

Intuit maintained group-level operating profit growth, supported by acquisitions and while certainly not a Visa or Microsoft in terms of resilience to downturns, Intuit performed much better than many other companies supporting the financial economy and those providing software to small businesses.

Beyond dealing with the crisis, Intuit, like many legacy software companies, was also dealing with the technology transition to mobile computing and the cloud, setting up for the Brad Smith era.

Phase 3 2008 - 2018. The Brad Smith era

Prior to his CEO promotion, Brad Smith initially led the accountants division at Intuit before leading both the consumer tax and small business (now called global business solutions) divisions, driving both revenue and market share growth during the five years.

If Steve Bennett brought stability, Brad Smith brought a growth culture to the group. Intuit’s challenge post its GE-era years was that it lacked innovation and the ability to scale new products to customers. Only 4 of the 50 products it launched in the prior decade grew above $50 million. Brad Smith immediately identified this, transitioning Intuit from a top-down R&D approach to bottom-up with smaller teams, sometimes as little as just two people.

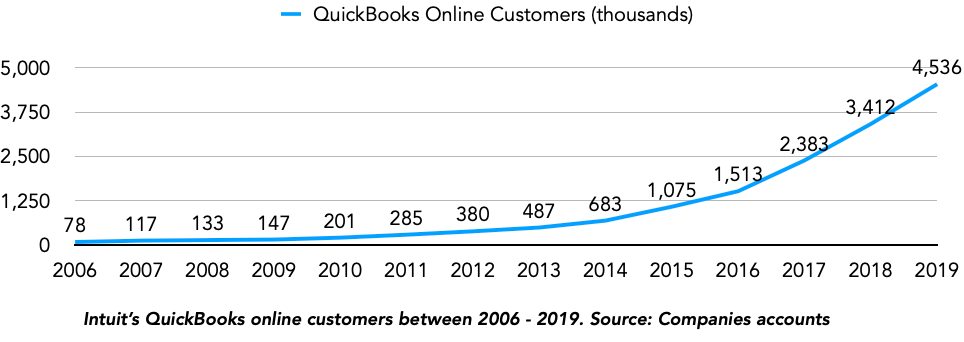

Intuit was also among the faster-moving legacy software companies with the transition to the cloud and mobile computing. QuickBooks users had historically upgraded every other year, but the cloud’s economics of transitioning QuickBooks to a more recurring monthly model incentivised Intuit during this period. For example, QuickBooks Online Plus was initially available for $34.95 per month, while Payroll for QuickBooks Online was priced at $19.95 per month.

“Usability is the hallmark of Intuit’s desktop accounting products, and the online version carries on that tradition. Overall, the design is exceptional; I like it better than what comes out of the box.” - PCMag.com Product review

The Brad Smith era was quite successful, with Intuit’s EBIT growing from $644 million to $1,560 million (9% CAGR), with its shares rising by 582% during the ten years.

Although market commentators painted the decade as a completely rosy period, Intuit still had some failures. Intuit had ignored the international market, focusing mainly on the U.S., which created an opportunity for Xero to win share and eventually leadership in key markets like the UK and Australia, among others.

Quicken continued to decline and struggle in the cloud world, leading to an eventual sale in 2016. Several products like SnapTax, QuickBase (low-code workflow builder), Intuit Health (bought in 2010, sold in 2019) and Intuit Homestead (website creation and hosting) were shut down. Despite these failures, Intuit still delivered profitability growth as progress across QuickBooks and TurboTax mattered more.

Phase 4 2018 - present. The Sasan Goodarzi era

After 10 years, the CEO role moved to Intuit’s current CEO, Sasan Goodarzi, a then 14-year Intuit veteran, having worked and led both the consumer tax and SMB units. Sasan inherited a very healthy Intuit, centred between both QuickBooks and TurboTax, and his goal was transitioning Intuit away from an “SMB + tax” into the financial operating system. Achieving this goal relied on two strategies: the acquisition path and the artificial and human intelligence strategy.

Acquisitions

Intuit has always had a soft spot for the consumer finance market, and to reenter the market after its sale of Quicken, Intuit acquired Credit Karma for $8.1 billion (10x revenue) in 2020. Unlike Quicken, Credit Karma is less focused on the bookkeeping aspect of consumer financing; rather, it’s more focused on the “lending marketplace” aspect and is somewhat diversified across credit cards, personal loans, insurance and auto loans. We will get deeper into its business and growth prospects, but overall, it’s clear Intuit overpaid for Credit Karma.

The second major acquisition was Mailchimp, and likely an even costlier mistake was acquiring the customer marketing software business for $12.1 billion (15x revenue) in 2021. Prior to Mailchimp, Intuit had various attempts in this market. Demandforce, acquired in 2012 but later sold two years later, supported SMB customer marketing and automation. The Homestead acquisition in 2007, which became Intuit Websites, addressed some of Mailchimp’s current services that struggled in the face of Wix and Shopify.

Artificial and human intelligence

The more successful strategy in the Sasan Goodarzi era has been merging both artificial and human intelligence for existing tools and solutions. On the human and tax side, TurboTax Live, initially launched in 2018, connected users with tax experts, filling a gap its chief rival, H&R Block, had over Intuit.

A year later, Intuit launched QuickBooks Live, similarly connecting SMBs with bookkeeping and accounting experts with a range of services. These solutions increased the network effects, customer experience and value chain relationships for Intuit and today, both continue to grow quite fast, strengthening Intuit’s overall moat.

To further deepen the financial ecosystem, there’s also been further prioritisation on cross-selling across the various products;

TurboTax and Credit Karma: Credit Karma users can directly file taxes through TurboTax in the Credit Karma app while TurboTax users have access to Credit Karma recommendations, driving commission and ad revenue. To further deepen this, Intuit officially merged both units in FY 2026 as the consumer segment.

QuickBooks and Mailchimp: Given both serve SMBs, bookkeeping QuickBooks users are often sent emails on ways Mailchimp could amplify their customer reach, and QuickBooks open architecture directly syncs both applications together.

To further strengthen this ecosystem model, Intuit’s culture under Sasan Goodarzi has also transitioned more to the open system architecture, similar to other larger and modern technology companies. Intuit discontinued bets it concluded it couldn’t win, integrating deeper with companies like Shopify, Square, Stripe and other AI-native apps.

Until the past year, the Sasan Goodarzi era had been successful from a revenue and operating profit growth and share price performance view, with earnings compounding by 17.9% CAGR and a share price return of 304% (24% CAGR); that was until its most recent 50% share price decline, which brings us to where we are today.

Wall Street has voiced its concerns for Intuit’s future in today’s AI-driven world, and as we have learned from reviewing its history, this isn’t the first or second time markets have been worried about Intuit’s future. It’s also dealt with several technological shifts. Despite initial struggles and failures at each, from the internet during Scott Cook’s latter years in the 1990s to Brad Smith’s mobile computing challenges in the early 2010s, Intuit survived each, and I believe this is due to how embedded it’s become for SMBs.

Before exploring its product suite and economics, let’s first discuss the markets Intuit operates in.

2. SMB Financial Services Industry

Intuit is a technological conglomerate operating in several vertical markets, and to best understand its competitive landscape and wider industry prospects, it’s best to break the industry analysis across the main areas. Within the financial services segment, Intuit operates in four verticals: accounting and bookkeeping software (QuickBooks), payroll, payments and customer marketing and outreach (Mailchimp).

Let’s first look at the largest of these four markets, the accounting and bookkeeping software industry.

Accounting and bookkeeping software