Visa Inc

The investment case in Visa (and Mastercard)

Due to the length of the Visa deep dive (70-pages), a PDF version and link to both Visa’s and Mastercard’s valuation models are provided at the end of the post. Premium readers can scroll to the end to read this deep dive on the PDF format.

Visa hardly needs an introduction. Its services (and Mastercard) are ubiquitous in payments. There’s a high chance you currently have 4 to 5 Visa or Mastercards in your wallet, averaging more than 30 card taps a month. Today, Visa is the 17th largest listed company globally (Mastercard is the 22nd largest). Its 50%+ net profit margins are well publicised with nearly 50 sell-side analysts covering its shares (42 rate it a buy, no sell).

Its shares have returned 22-fold (19.3% CAGR) since going public in 2008 and currently trade at a rich 23.2x forward P/E based on market consensus earnings projection.

What possible upside could Visa offer given its coverage and well-known business model?

On closer inspection and research, I realised Visa had a lot more to offer than just a payment network that collects fees when we tap.

While national real-time payment systems like PIX (Brazil), UPI (India), cannibalise their transaction revenue, they offer Visa a unique opportunity in Value Added Services (VAS), particularly in tokenisation and real-time fraud risk.

Since consolidating Visa Europe Ltd into Visa Inc, it has intensified its growth in cross-border transactions, which have a higher margin than domestic transactions.

Agentic commerce, where AI agents discover and purchase products on our behalf without human “payment tapping,” could spur even more growth for Visa’s network and technology stack.

Despite its quality and track record, Visa has underperformed the S&P 500 in the last 1,3,5,7 years, and given the recent share price weakness, it’s a great time to revisit the Visa investment case, and I’ll explain my thought process behind my recent investment in its shares.

Note, there’s no studying Visa without Mastercard, and upon further study into Mastercard, its recent drawdown made its shares undervalued and above our IRR target, and I also purchased some shares during the research. You can also find Mastercard’s valuation model in the valuation section.

Market capitalisation (As of 24th February 2026): $585.6 billion

Jenga IP 2030 FY estimated market cap: $1.03 trillion

Potential IRR (including dividends and buybacks): 16.4%

Jenga IP Quality Rating: 85.8/100

Here’s what I’ll cover:

History of Visa Inc: An overview of its creation within Bank of America, its mutualisation and later demutualisation, and how both shaped its moat and business quality today. Efficiencies gained post its IPO and case studies of Visa’s ability to withstand financial crisis, technological shifts and regulatory shocks.

Overview and analysis of the Global Payments Infrastructure: Analysis of the global payment infrastructure, overview of key players (issuers, acquirers, networks, processors and gateways), consumer to banks supply chain analysis, a comparison of payment networks by payment volume and transactions, the payments industry by type (credit, debit, bills), the growth of cross border payments, the value-added service market opportunity and how recent innovations like Buy Now, Pay Later (BNPL), agentic commerce, cryptocurrencies, A2A and national payment systems impact the open network model.

Visa versus Mastercard comparison: An up close comparison of the two largest open payment networks, market share across geographies, key business economics differences, growth and cost drivers, an overview of their products and service portfolio and acquisitions strategy.

Business economics of Visa: A deep dive into Visa’s core revenue lines (service, data processing, international and other), revenue by region (U.S. and international), KPIs and an assessment of network fees and value-added services over the years. Analysis of its cost structure, efficiencies gained over the years, state of its legal and litigation liabilities and a deep dive into its unit economics across various transaction types (debit, credit, cross-border, commercial, BNPL on rails and A2A).

Growth potential: Analysis of its growth drivers in applications like e-commerce and agentic commerce, real-time and push payments, cross-border (B2B transactions and remittance) and insights into countries with growth potential (yield and volume changes).

Risk and challenges: Further assessment of Visa’s relationship with governments, current litigation liabilities and pending cases, further analysis into the rise of national payment systems, operational and growth gaps to Mastercard, the ongoing credit card caps in the U.S., and the Big Tech threat.

Visa’s Valuation: An earnings multiples-led valuation and projection of its earnings potential through to 2030 FY, comparison with peers and the broader payments industry.

Mastercard’s valuation: Assessment of Mastercard’s business economics, earnings growth and valuation through to 2030.

Conclusion: The 30x P/E club - being a value investor in high P/E companies.

1. History of Visa Inc

Some of the greatest companies have been created internally within large financial services companies (MSCI, BlackRock, Morgan Stanley). Some other greats were created when industry participants consolidated as the shareholders (Airbus, Amadeus IT, ICE), while others needed to experience early near-death challenges to become great (FedEx, Intuit, Nike).

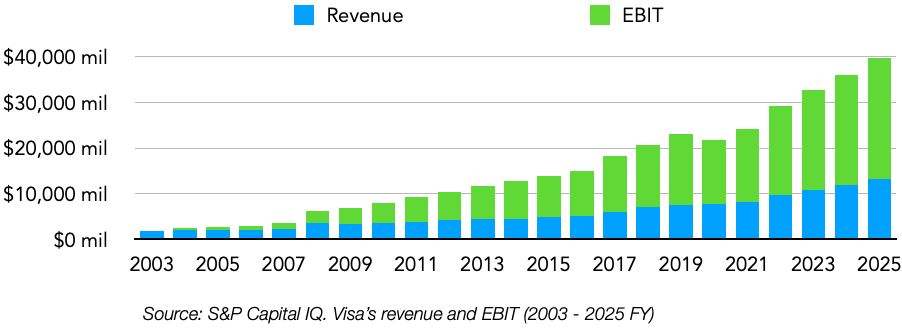

Visa went through all three experiences, which shaped its business quality and moat as we know it today, and to understand how it became a $590 billion company, achieving $40 billion in revenue annually, we must first understand the payments problem pre-Visa and how it solved it.

Payments Pre-Visa (-1958)

Payments and the transfer of money for goods and services without using actual cash had been around for decades, pre-Visa (1958), initially in the form of cheques, then the creation of the Federal Reserve in 1913 and clearing houses increased non-cash alternatives. Before credit cards as we know them today, companies had developed charge cards, that is, credit cards between a customer and a merchant that only needed to be repaid at month-end, saving time and effort paying cash for each transaction.

By nature, high volume and necessity services like travel, retail and fuel stations capitalised on these, and the charge cards increased customer loyalty and sales, given the transaction cost savings when compared to cheques. However, the charge cards didn’t scale as they were often limited to the higher-income households, and they also lacked a “one card fits all” approach.

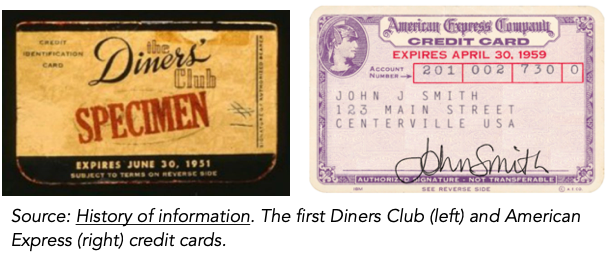

These two challenges created an opportunity for charge cards with multiple applications, led by Diners Club (current 4th largest payment network) in 1950 and American Express (current 3rd largest payment network) in 1958. Both companies, while similar (American Express once attempted to buy Diners Club), pursued different growth strategies. Diners Club had initially focused on restaurant payments before diversifying into other applications, while American Express broadened across global travel and more affluent consumers.

Despite their profitability, less than 5% of Americans had one, and their high merchant fees caused tensions between them and merchants, leading to slow adoption. Banks recognised this issue and attempted to address the market gap, serving the middle-class with a revolving credit facility, meaning you no longer needed to repay merchants at month-end.

BankAmericard to Visa (1958 - 1976)

Before the creation of Visa, initially called BankAmericard by Bank of America, several other banks, such as Flatbush National Bank of Brooklyn in 1947, experimented with credit cards, but as we’ve learned in several other company deep dives, the first to market doesn’t always result in long-term success. The key challenge many faced was scale. During those years, most states limited banks from operating multiple branches or entering new states, curbing their growth. Like all “network-based” business models, achieving scale quickly is critical.

Bank of America, then only in California, was the largest bank in the U.S. and was also the first to integrate technology into its operations, tested its credit cards in 1958 in Fresno, California. A mixture of unsolicited and aggressive marketing (a key component of Visa’s success, as we’ll discuss later) led to success here, but due to fears of competition from other banks, they aggressively expanded across the state, adding 2 million BankAmericards in a year.

Common to many cases of aggressive credit growth, Bank of America faced high delinquencies and would take years to recover from these losses. By 1961, it became profitable, and to gain nationwide scale, they created a license model, partnering with banks in other states for a fee (initially $25,000) and a percentage of transactions as royalty. While this brought scale, there were two other challenges for Visa, which I believe are the second and third pillars of Visa’s business model: combating fraud and building trust.

Fraud: In the early years, cash remained king simply due to the fraudulent transactions and slow technology in BankAmericard’s process. For example, merchant authorisation could take 5 to 20 minutes, and transactions below a certain value ($50 or $100) didn’t need to be flagged during the authorisation. Once fraudsters figured out the limit, they transacted just below it to avoid getting flagged.

While there’s no official figure, it’s estimated that the Bank Credit Card fraud had reached $116 million, with issuers being the biggest losers. To combat fraud and reduce processing time, the BankAmericard team, led by its new CEO, Dee Ward Hock, created the BankAmericard Service Exchange (BASE 1), which transitioned the system from paper-based to electronic, cutting the authorisation time to less than a minute.

Trust: Given that Bank of America still retained the ownership and power over the licensees, there was distrust towards the parent company, as many feared potential competition. Participants also distrusted one another, given that there wasn’t a unified system and that it had inconsistent chargeback rules. Dee Hock and the rest of the team were forced to make several changes. Coupled with technological improvements to the network, members were provided quarterly reports, highlighting the performance of members and provided support to underperforming members.

Second, BankAmericard doubled down on marketing and educating cardholders (and the government) on its benefits, steering the message away from credit and more towards “a medium of exchange”. Finally, to further disassociate from its parent, Americard was renamed Visa Inc (1976), and to decentralise global operations, the company was reorganised into five semi-autonomous regions, with each setting its own operating regulations.

The competing interests, technology hurdles, scale and trust required to create a Visa Inc network, as we know it today, is central to the investment case today, a high quality and moat business. The nature of the business model meant there could only be a handful of participants. In fact, the core reason behind the creation of Mastercard, initially called Interbank Card Association (ICA) in 1966, was to neutralise the growing power of Visa by banks that didn’t want to cooperate with Americard.

Led by Karl Hinke, Mastercard’s first CEO and then Marine Midland Bank (a New York bank that BankAmericard had rejected as it was too big) created the association in 1966, renaming it to MasterCharge in 1967 and then Mastercard a decade later.

Technology and debit card transformation (1976 to 2006)

While it would be informative to assess the 30 years during Visa’s history, there are three key innovations and themes I want to highlight from this period that deepened Visa’s moat for the future: VisaNet, Internationalisation and Visa debit.

VisaNet: Visa’s network purpose is to authorise, settle and clear payment transactions at real-time speed. Dee Hock’s priority was ensuring real-time authorisation, which was achieved with Base 1 (discussed above), and the next phase was improving the speed in both the clearing and settlement steps (known as Base 2) via building the largest automated clearinghouse. Rather than settling transactions with one another, the member banks now settle with only the clearinghouse, saving significant time (from 6-8 days to overnight clearing) and costs ($15 million in cost savings in year 1).

Visa invested in several technologies and partnerships with technology companies like IBM to achieve Base 2. As transaction volume grew, Visa invested in more data centres and processing capacity to keep up with demand. Later innovations such as integrated payments, tokenisation, contactless cards and 3-D Secure were layered on top of VisaNet. Each of these were important as they reshaped Visa from just credit processing to a financial technology platform.

Internationalisation: To be truly global as its ambitions stated, Visa needed to ensure cardholders could use their credit cards in foreign countries and settle in multiple currencies without further delays or additional costs. Visa created an “auto-telex” system that linked to Base 1 to make this possible, with the first links to the UK and Canada in 1977.

Over the next decade, Visa invested in many leased lines and satellites to connect to all its global members, before then replacing the technology with its own private computer network. On the multi-currency front, Mastercard had moved earlier than Visa with its partnership with Eurocard in the 1980s. In response, Visa stepped up its efforts and by 1986, with the support of Barclays Bank, Visa began offering multi-currency settling, shaping up for global growth.

Visa Debit: Contrary to popular belief, Visa’s management aim wasn’t to popularise credit cards, but rather, create a technology infrastructure that served as the means of financial exchange. Visa began researching its first international debit card in 1973, initially called an asset card, as it would access deposits and investments.

Although the benefits to consumers were quite obvious, the debit card technology was unpopular among member banks because it was seen to cannibalise the already existing ATM operations. However, Visa had already built the infrastructure via the millions of terminals, and once it became obvious that the queuing time savings at grocery and retail stores when purchasing with debit cards (then called check cards), it quickly became integral to payments, surpassing credit card payments for Visa by 2003.

Why these matter today: Three pillars of the Jenga IP Quality Index are barriers to entry, nature of demand and market & growth opportunity and each of these three factors during the 30 years cemented Visa’s overall moat, and I’ll briefly discuss how.

Barriers to entry (financial technology): Visa scores 8.85/10 on the barriers to entry quality category, the highest among all companies deep dived, and a key reason for this was Dee Hock’s technology-first mindset that shifted Visa from just a banking credit extension to an infrastructure built on the latest innovations.

Today, the payment network market is tightly held among the same 5 networks created in the 1960s, and the only real potential new entrants are governments that build national payment infrastructure, as with India and Brazil.

Market and growth opportunity (Internationalisation): Focusing on the global opportunity, rather than just the U.S., not only cemented the barriers to entry but also increased its growth and market opportunity. Since 2017, after it reconsolidated Visa Europe under Visa Inc, it has made more revenue from its international markets and cross-border payments, a sub-market that had been impossible until the late 2000s, now serves as a key growth opportunity we’ll discuss later.

Nature of demand (Visa debit): Although credit is more profitable given its higher take rate to the payment network, consumer debit (and also commercial) have been important products in making Visa’s volumes less cyclical and more durable to economic shocks.

Litigations and more litigations (2006 - present)

Even though there were several competing networks, Visa held nearly 60% of all payment transactions by 2006 globally, earning $3.9 billion from $3.2 trillion of payment volume. Its scale, penetration, profitability and influence have led to some key philosophical questions among the investment community, regulators, merchants and partners:

Why should Visa Inc, a mutually owned company, earn profits?

Is the value provided by its payment rails equal to the ‘tax’ it levies on global commerce?

Does a private company hold more economic power over a nation’s central bank?

Is Visa’s mutual ownership unfair to competition?

While I have my views on each, it’s more important to reflect on how its stakeholders have answered and responded to these questions over the years:

Competition (Mastercard, American Express and Diners): While regulators have historically grouped both Mastercard and Visa as the antagonists, Visa’s earliest form of anti-competitive behaviour was actually towards Mastercard, when it prohibited its member banks from issuing competing cards, specifically those from Mastercard. It wasn’t until one of its members, Worthen Bank and Trust, sued Visa that this issue was taken more seriously.

Six years later, in 1976, courts ruled the exclusive dealing illegal, leading to an era of “duality” where local banks could issue both Visa and Mastercards. While this solved the issue, it created another challenge - Visa and MasterCard combined versus the rest (Diners Club and American Express).

For the initial years, the battles were fought in commercials and marketing, but the late 1990s saw a turn when the U.S. Department of Justice revived an investigation into the effects of duality and exclusivity rules that had prevented others like Amex from partnering with banks. The results of this investigation led to the IPO’s of both Visa and MasterCard and also financial payouts (Visa $2.3 billion, Mastercard $1.8 billion) to American Express and billions to Discover as well.

Governments (U.S., EU, Australia, Brazil and India): The U.S. government’s scrutiny of Visa initially started from increasing competition and innovation among payment networks, but over time, it has broadened into its overall market power across debit transaction routing and mergers. Beyond its domestic government, others, particularly in Europe, Australia and the BRICs countries, have further clamped down and scrutinised Visa’s power from interchange and cross-border fees (Europe, Australia and Canada) to payments sovereignty (Brazil, Russia, India and China).

So far, there have been two types of losses for Visa. Countries that used technology to fight back (Brazil and India with their alternative payment infrastructure) and countries that were aggressive on the regulatory front (the EU and Australia) by capping interchange fees.

Merchants (Walmart, Target and Home Depot): Visa’s core business strategy is keeping everything within its rails and has employed several tactics to achieve this. Merchants (led by airlines and retailers) pay interchange fees set by the card networks and are most incentivised for interchange fee reductions. Led by Walmart, there have been several class action lawsuits on reducing interchange fees and also limiting Visa’s power, such as the tying arrangement, which forced merchants that accepted Visa credit to also accept Visa debit cards. More recently, there’s been further lawsuits on more operational changes, such as the Walmart’s PIN versus Signature debit routing case.

Issuers and acquirers: Unlike the other three stakeholders, issuers and merchant banks are less incentivised to legally challenge Visa’s and Mastercard’s as they also benefit from higher interchange fees and are deeply integrated partners to the networks. The tensions tend to be more commercial than litigation and are usually privately settled either with incentives or with issuer losses to an alternative network, as we saw with NatWest in the UK and CIBC in Canada.

The immediate cost for Visa in these numerous legal issues is the billions it’s paid out in litigation expenses over the past two decades. Another key impact was its demutualisation and transition into a publicly listed company, following Mastercard’s decision.

Visa Going public

To raise additional capital for the then ongoing regulatory and legal challenges, Visa followed Mastercard’s footsteps, raising $19.7 billion, becoming the then largest U.S. IPO. The transition to a publicly listed company marked a new phase for Visa as it transitioned ownership from banks to public shareholders, while also protecting the latter group from the incoming wave of legal costs. For banks, the IPO was also important as it helped them raise some capital to support liquidity during the financial crisis - JP Morgan Chase made $1.3 billion as the largest selling shareholder.

The more important by-product of the IPO were the efficiencies gained.

Utility to for-profit culture: Although the non-profit mutual ownership structure at Visa had its benefits, to keep up with the already public Mastercard and the changing payment landscape, Visa had to transition from its mutual ownership because the old structure significantly slowed decision-making and limited Visa’s financial power to invest in growth opportunities.

With the additional money raised, Visa mapped a clear for-profit cultural shift, eliminating the many regional boards, shifting from a region to country-level decision-making process, limiting bureaucracy, and also broadening its partnerships beyond previous member banks.

Global expansion: With Visa Inc (excluding Visa Europe) now consolidated into one entity, management led by its then CEO, Joe Saunders, Visa stepped up its global expansion, particularly in emerging markets (Brazil, South Africa and Thailand) and made its priority of more than 50% of revenue coming from countries outside the U.S. At the time of its IPO, cross-border payments was flagged as a high growth market (a then $11 trillion market opportunity) and Visa invested aggressively to catch up with Mastercard in its VisaNet technology, to support cross-border and remittance payments.

By 2010, Visa Money Transfer was already present in 15 countries. The acquisition of Visa Europe in 2016, which wouldn’t have been possible under its old structure, further turbocharged Visa’s global strategy.

Faster innovation: Although innovation was central to Visa’s strategy as we discussed, the rise of mobile, e-commerce and additional fraud risks meant Visa had to move even faster with launching new services, particularly in the value-added service segment, an area its banking partners were unsupportive of, as these services competed directly with issuers and banks. Visa achieved further innovation in two main ways.

First, with the simplified board and operational structure, Visa launched new services like Visa IntelliLink and advanced authorisation tools to support commercial and consumer end-use cases, respectively. Several products like Rightcliq by Visa were launched to support the fast-growing e-commerce market, and several solutions for the growing smartphone market, like transaction alerts and mobile contactless payments.

Second, acquisitions, which were nearly impossible under the old structure, became increasingly important for Visa. Within its first three years as a listed company, Visa acquired Fundamo, PlaySpan and Cybersource to further boost its solutions in its three growth opportunities (mobile, e-commerce and security & fraud solutions).

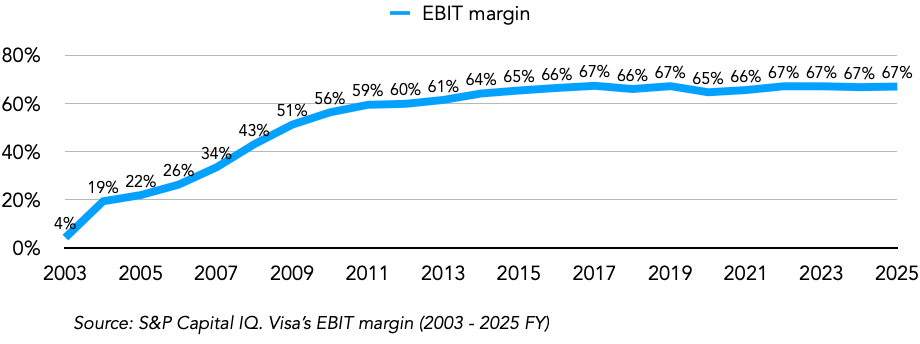

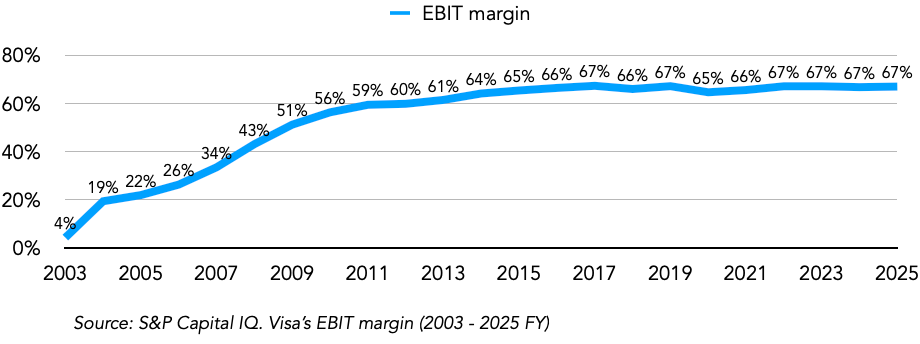

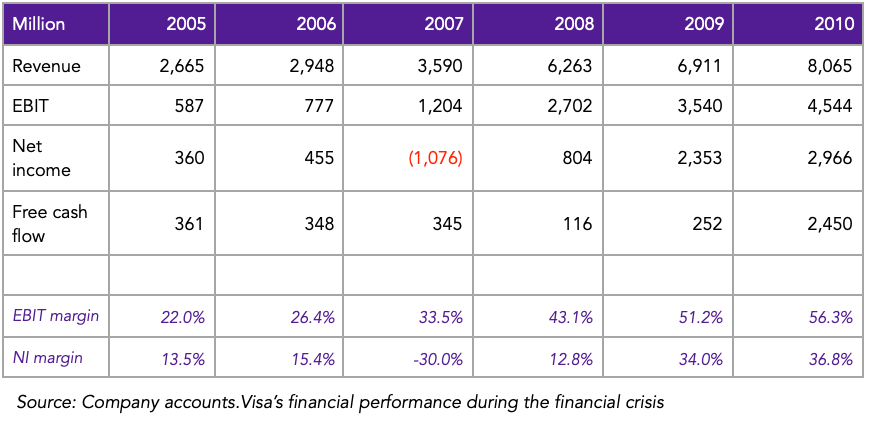

As the EBIT margin chart above portrays, the many operational changes post its IPO led to its EBIT margin increasing from 34% in 2007 to 59% in 2011. More impressively, the margin expansion was also during the volatile financial crisis years, a period when travel and financial transactions slowed.

Case study: Visa Inc during the financial crisis

Every crisis is different, but studying how companies survived and operated during crisis mode does present clues on their business resilience and ability to withstand shocks.

Unlike banks and other financial institutions, Visa doesn’t take on lending or depositary risks with its balance sheet, keeping its economics and financial profile naturally much less risky than its peers. That said, there’s still some exposure, particularly in the credit and cross-border segment. Given that Mastercard is more exposed to both segments, one tends to see a steeper economic decline at Mastercard during economic shocks, but a faster rebound coming out of the downturn.

U.S. credit growth: The credit growth initially fell to single digits before turning negative in the final quarter of 2008

U.S. debit growth: Visa maintained its double-digit growth in its home country and in international markets in the more resilient debit card segment.

Cross-border: Visa’s growth fell across all regions, given the decline in travel and remittance payments.

“To put cross-border payment volume in historical context, in the recessionary period of late 2001 and early 2002, monthly payment volume growth fell to low single digits and there were several months that were slightly negative” - Visa Q4 2008 earnings call, Byron Pollitt, former Visa Inc CFO.

Another key element of Visa’s financial profile is its balanced geographic exposure, which came in handy during the financial crisis, as non-U.S payments represented more than half of its 2009 FY payments volume.

The one geography Visa doesn’t have much of a direct presence, at least until recently, is China, but before unravelling its operations today, it’s worth exploring the broader payments industry, key players and how payments actually work.

2. Overview and analysis of the Global Payments Industry

There are different viewpoints at which one might assess the global payments industry, whether by source of payment (debit, credit or prepaid), method of payment (cash, card payment or Account-to-Account) or by application, goods and service purchase, bills, remittance, among others.

To truly have an in-depth understanding of who the key players, what direction the global payments industry is heading into and which markets and segments either face long term growth opportunities or headwinds, its important to study to payments industry from the various viewpoints but let’s first establish the anatomy of the payment industry, who the key players are and how Visa and Mastercard fits into the payments infrastructure.

Anatomy of the global payments industry

Visa processes over 300 billion transactions globally, and as consumers, these transactions are completed within the blink of an eye. While technology and payment networks play a key role in the process, there are several other relevant parties in a payment transaction.