Software Continued

The Foundational Five Dominance

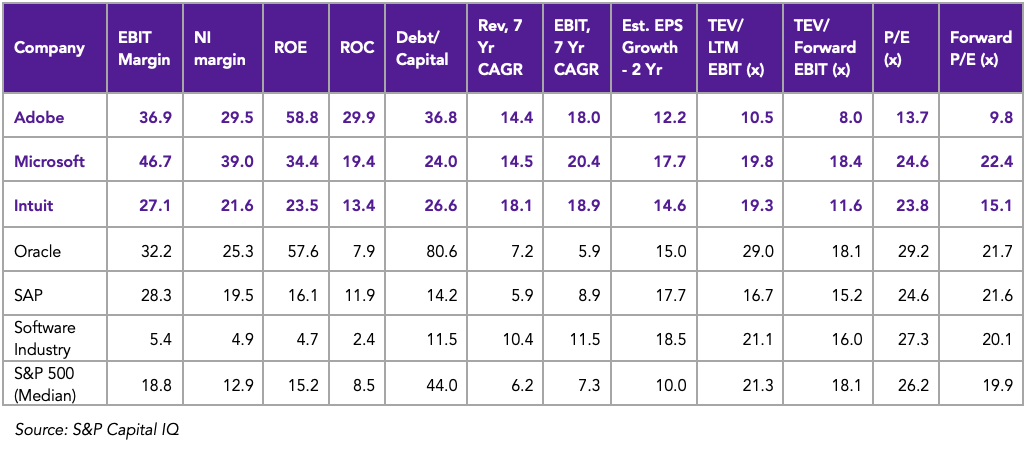

While digging into Microsoft over the past month, some insights particularly stood out, and one of these was the staying power of software once they become embedded into workflows. There’s a group of five listed companies founded between 1972 and 1983 that best exemplify this: Microsoft, SAP, Oracle, Adobe and Intuit, what I call the foundational five software companies.

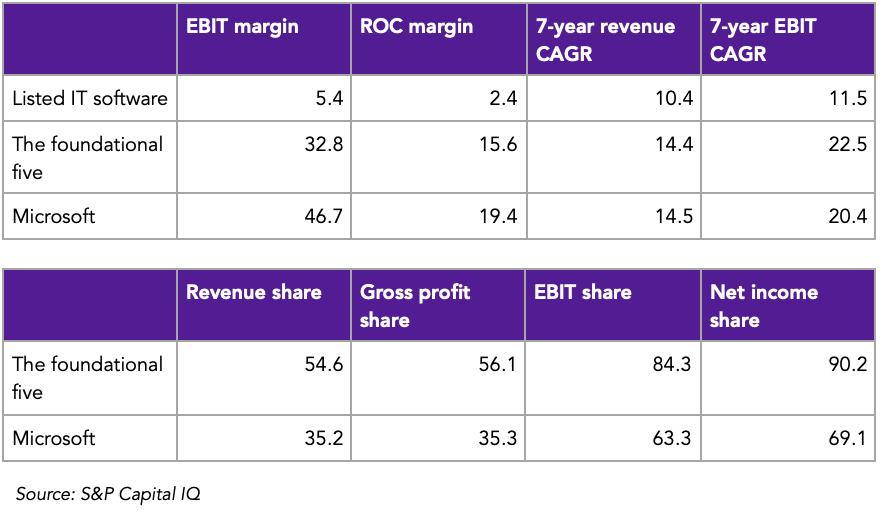

To highlight their dominance, the tables below compare the foundational five companies with the 773 listed IT software companies (GICS).

As highlighted in the table, the foundational five companies achieve EBIT margins (32.8%) 6 times greater than the listed IT software industry and surprisingly, they also achieved faster revenue and operating profits growth over the past seven years, with their 7-year EBIT growth being twice as fast as the industry, despite their size.

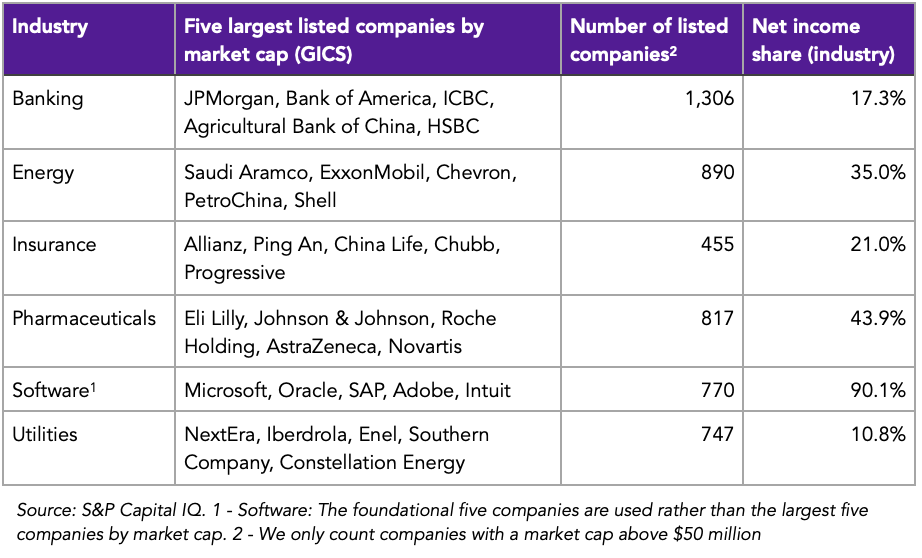

The second table contains one datapoint I want to focus on a bit, their share of the industry’s net income, currently at 90.2%. This highlights how oligopolistic and winner-take-most software is. While some might argue this is normal for a mature industry, no other industry comes close to this level of concentration from a public market’s perspective.

The table above compares the share of net income the largest five companies represent, and as you see, the next highest concentration is pharmaceuticals at 43.9% share, still less than half of software’s 90.1% share. Software may be the most winner-take-most industry and the real question today is to what extent and if AI breaks this structure.

A reasonable pushback is that a significant portion of Microsoft’s profits comes from cloud services, which arguably sit outside traditional software. Even excluding Microsoft entirely from the dataset, the remaining four companies still account for 74% of IT software net income, well above any other industry.

Adobe and Intuit

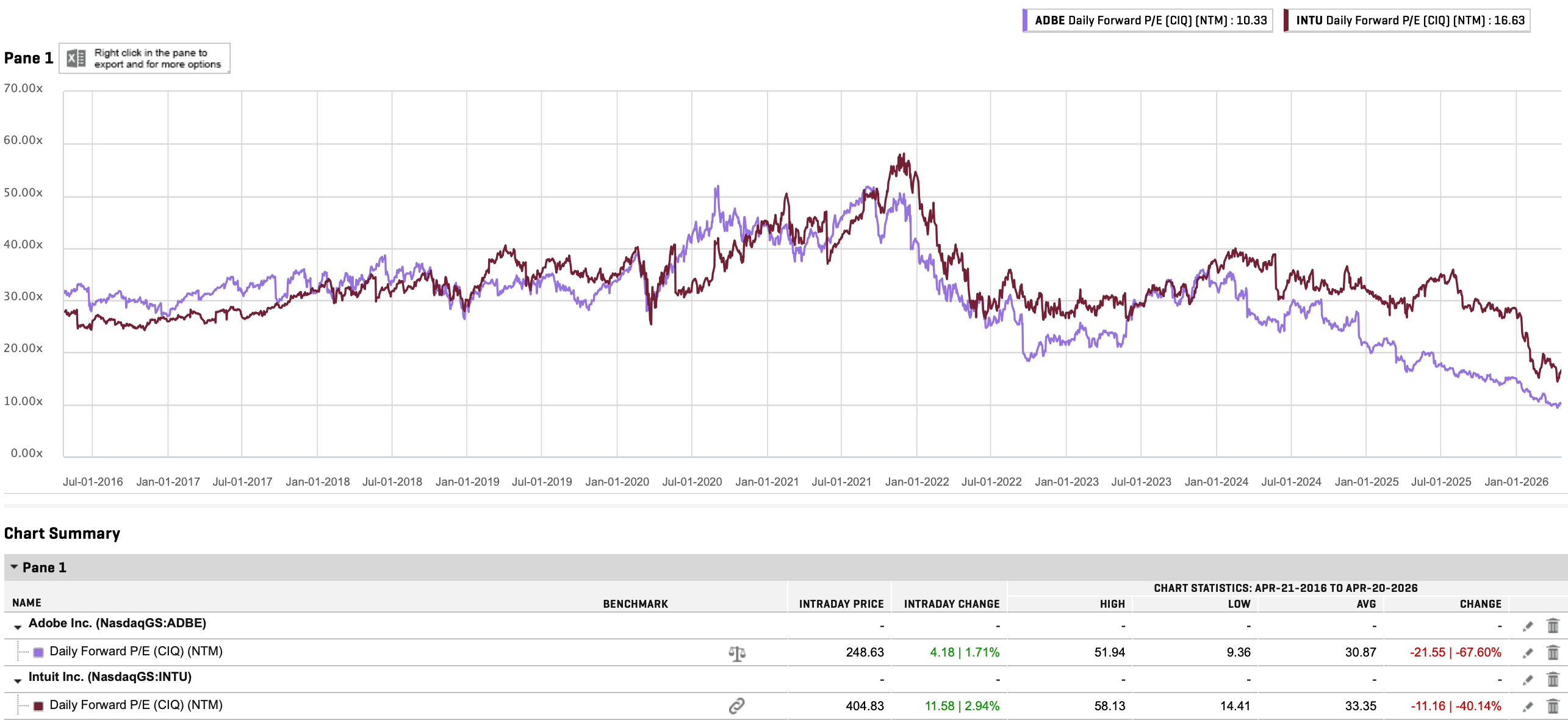

Until recently, the five companies seemed indestructible, with both Adobe and Intuit’s forward P/E exceeding 50x in 2021.

The AI challenge has brought a needed reality check to their valuations; Adobe, for example, declined to a 20-year low forward P/E of 9.8x while Intuit, for the first time since 2009, trades at a forward P/E discount to the S&P 500 Index.

Over the next few weeks, I’ll be spending some time researching both companies in-depth and will publish deep dives, starting with Intuit.

At the moment, I only own shares in Microsoft among the five companies and given how exposed the portfolio is to potentially at risk from AI companies (Microsoft, Visa, Mastercard and FactSet - 30% weighting), I’m raising my investment IRR hurdle from 15% to 25% for new software investments.

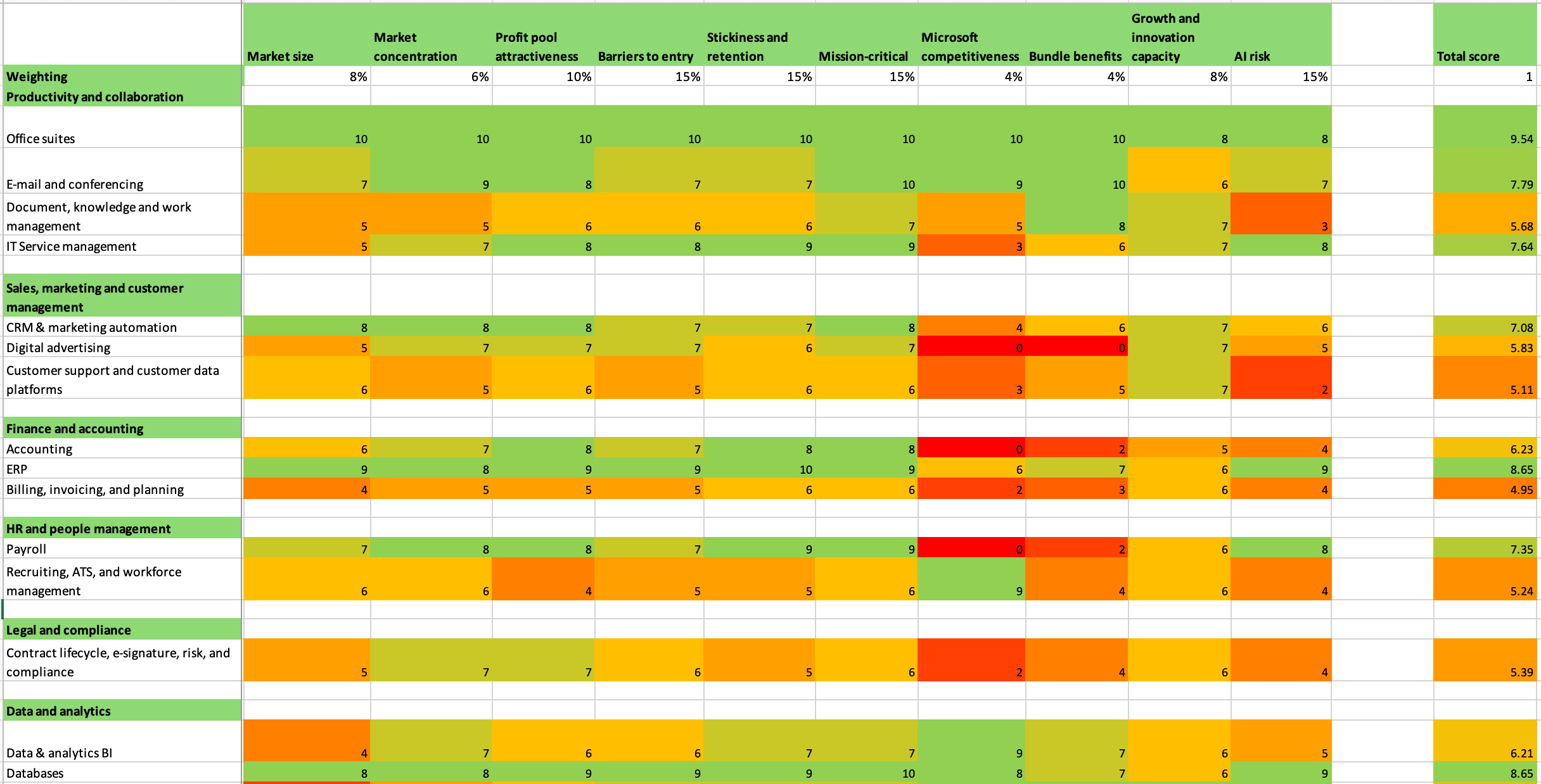

Beyond these companies, there are a few other companies on my watchlist, due for further research. During the Microsoft deep dive, I created a top-down overview of software, splitting the industry into 42 sub-industries and ranking them on key attributes like barriers to entry and market concentration.

Some of the watchlisted to-be-deep-dived-if-the-price-becomes-attractive companies include ServiceNow, Fortinet and Salesforce.

Finally, I’m also working my way through all 773 listed IT software companies from A-Australia to U-United States. If any other interesting companies that I understand, can value and seem to have favourable risk/reward come up, you can expect to receive additional research on them.

Difficult to imagine how far the "AI challenge" will impact the Software companies over the long term.

The sharp drop in fwd P/E values is a forewarning that should instigate a "strategy challenge" for these companies, to counteract the market realities. Perhaps it is to these strategies that the investor should pay close attention in examining these company's updated corporate information and actions