Visa Inc update

American Express enters the chat

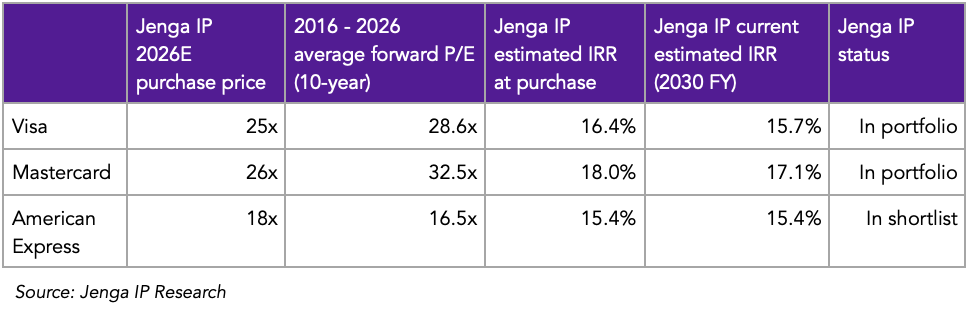

After spending most of my Q1 2026 studying the global payment networks, I concluded on the price range I’d pay today for each of the three networks:

Visa (25x my 2026 estimated net earnings)

Mastercard (26x my 2026 estimated net earnings)

American Express (18x my 2026 estimated net earnings)

Combined with EPS growth and dividends, I concluded that buying at the purchase multiples above could meet a minimum 5-year IRR of 15% (or a double in 5 years).

At the start of the research, only Visa met this target, but during the research, Mastercard joined the list through a combination of its share price decline and my improved understanding of its growth potential. Combined, both Mastercard and Visa currently make up 13% of the Jenga Global Fund.

You can read the Visa deep dive here.

At the start of the year, American Express, then a 25x P/E stock, well-above the 18x 2026E purchase multiple I assigned, was far off the buy range and given the then sentiment for its shares, it seemed likely to remain elevated.

Unexpectedly, the sentiment has quickly shifted, and its shares have declined by -21% in two months and now sit within my minimum 15% IRR target.

“American Express shares derated YTD due to the impact of the Trump administration’s proposed 10% cap on credit cards, and a potential impact of agentic commerce on the existing payment infrastructure. I discuss both topics in the Visa deep dive.”

So what am I doing with this information?

Portfolio management

For now, nothing.

While I’m optimistic about the resilience and prosperity of the payment networks, making them more than 15% of the Fund also wouldn’t be prudent from a portfolio risk management lens.

American Express requires more margin of safety due to its higher exposure to the consumer credit cycle, unlike Visa and Mastercard.

I’m also not a fan of too much portfolio activity, and at current prices, the risk/reward between Visa/Mastercard and Amex isn’t wide enough to justify reducing shares in the former to include Amex in the portfolio.

That said, there’s a price and an IRR difference I concluded justifies making changes here, a 10% IRR difference.

An example is if Visa’s shares rise into a 10% IRR potential ($404 per share, from $314 today), while Amex declines even further from today into a 20% IRR potential ($259 per share, from $303 today), thus leading to a 10% IRR difference between Visa and Amex.

Portfolios always face opportunity costs, and over time, I’ve come to learn the importance of factoring this cost when making investment and portfolio decisions.

So for now, I’ll be maintaining the current portfolio weighting while spending more time learning even more about American Express and stress testing current business and earnings growth assumptions.