Transport Infrastructure

A year later

A year ago, I made the investment case for several transport infrastructure companies around the world: airports, ports, railroads and highways. Unglamorous industries that make quite boring deep dives.

I first discussed the airport business model and then laid out the investment case for 2 of 3 Mexican airports (OMA and ASUR).

A month later, in June 2025, I discussed why I was bullish on International Container Terminal, a Philippines port operator and also discussed why Airports of Thailand was ripe for a rebound in my mid-year Global Equities report.

Finally, I curated a list of 10 transport infrastructure companies in the final reflections article that I thought were high quality and attractive valuations.

So have they since performed?

Not too bad!

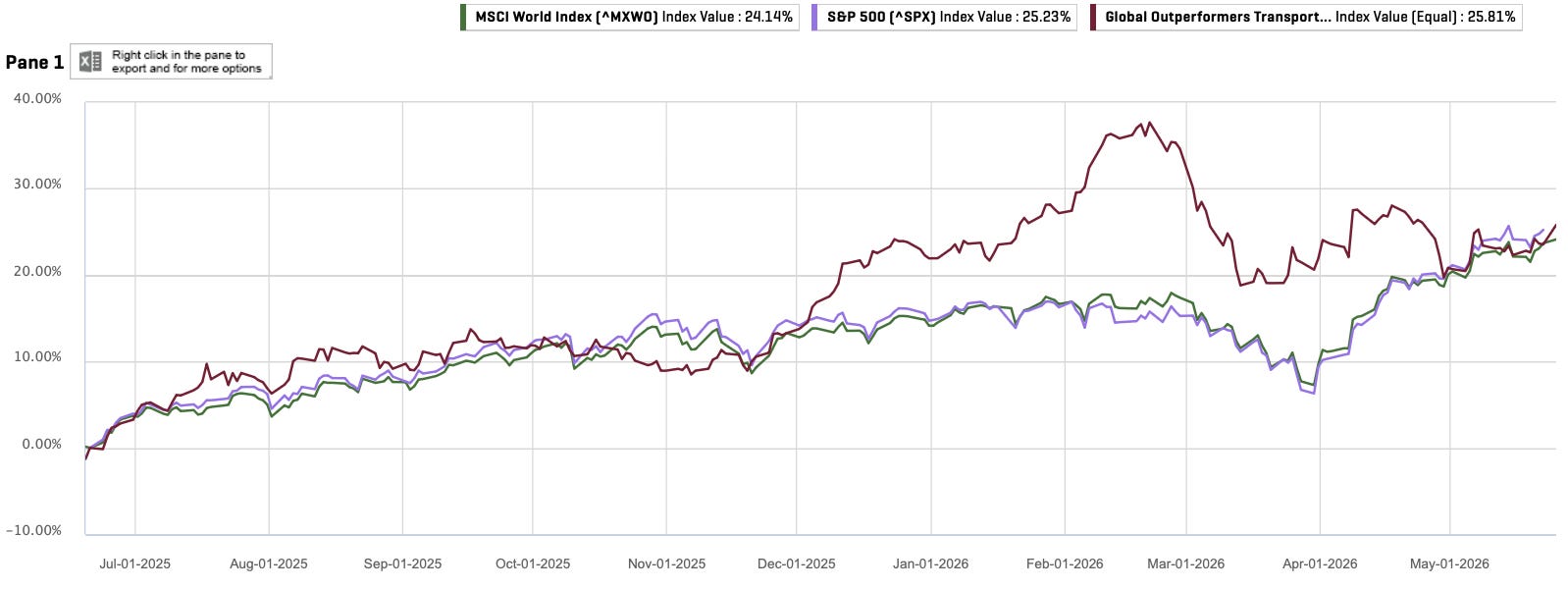

An equally weighted portfolio of the ten companies I recommended returned +27.1% (or +29.2% with dividends included), marginally above both the S&P 500 (+25.2%) and the MSCI World Index (+24%).

Interestingly, just before the Strait of Hormuz crisis in mid-February earlier this year, the transport infrastructure portfolio was roughly 20 percentage points (37.4% versus 17%) above the market benchmarks.

This is a reminder of the inherent risks in transport infrastructure. Despite being high barrier to entry assets, disruptions to the flow of goods and people directly impact their valuation sentiment and fundamentals.

Returns contributors

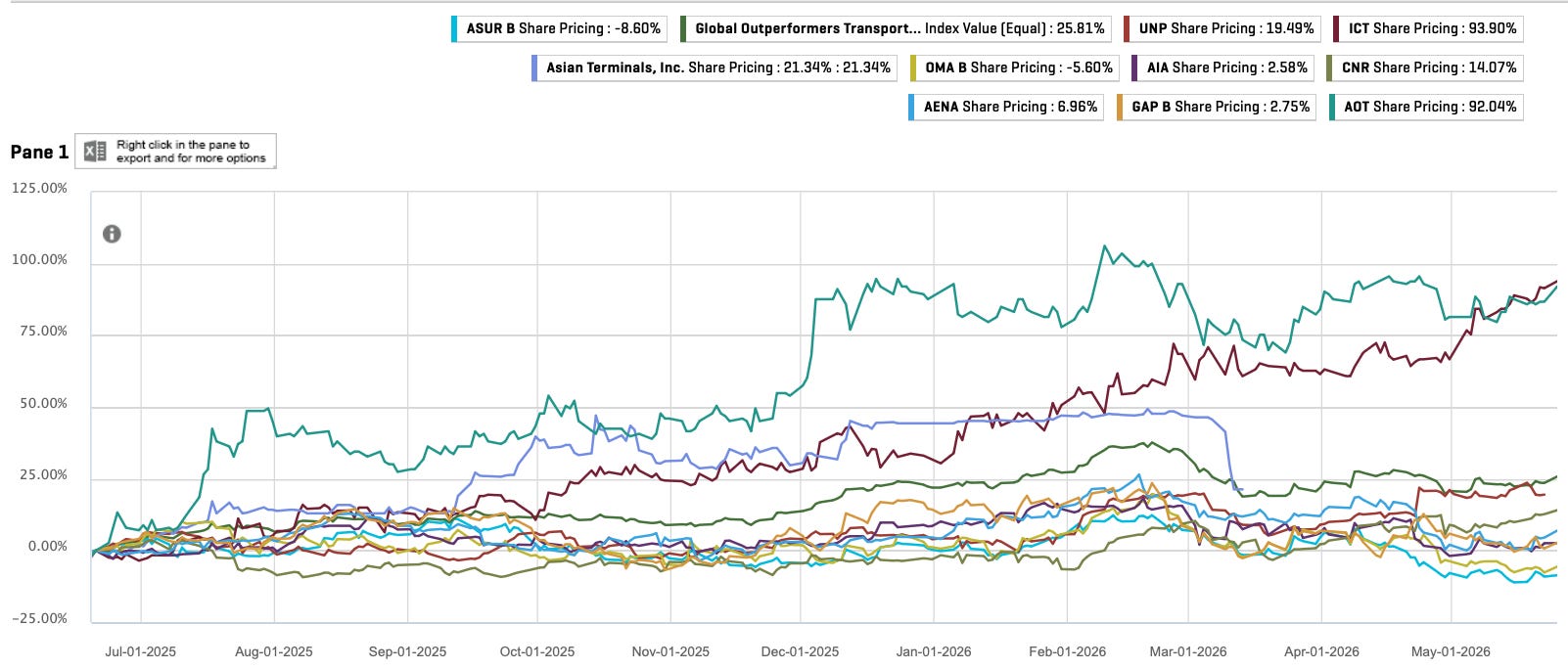

Class A (good): The portfolio was led by two significant contributors, ICTSI (+94%) and Airports of Thailand (+92%).

Class B (average): The rest of the returns were more muted. Three produced satisfactory returns: Asian Terminals (+21%) (now gone private) and the two North American railroad companies, Union Pacific (+19%) and Canadian National Railway Company (+14%).

Class C (bad): There were two negative performing companies, ASUR B (-9%) and OMA B (-6%), while three returned single digits; Aena (7%), Athens International Airport (+3%) and GAP B (+3%).

As you might notice, the majority of the transport infrastructure gains came from two companies, while the losses weren’t too severe, thus ensuring the whole portfolio remained resilient.

Beyond the 10 companies I shortlisted, there are 197 other listed transport infrastructure companies (GICS definition) above a market cap of $50 million. While we identified two top winners, there are a couple of others worth highlighting.

Emerging and frontier winners

One of the conclusions we had from the deep dives last year was that transport infrastructure is one of the very few industries in which emerging and frontier markets do better than developed markets. This is mainly due to the natural currency hedge and pricing power potential in emerging and frontier markets when compared to the more regulated developed markets.

Nigeria - Sky Aviation (+160%) and Nigerian Aviation (+149%)

I am embarrassed to mention that two of the top performers were Nigerian airport logistics companies. Despite being Nigerian, travelling there earlier last year, meeting management at both companies, and even discussing both in the same article where I shortlisted the 10 companies, I missed both companies and shareholders more than tripled their return in USD terms.

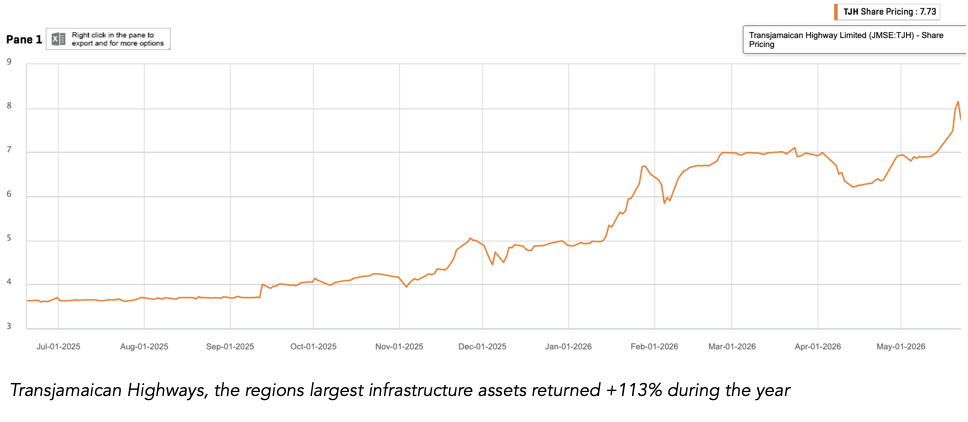

Jamaica - Transjamaican Highway (+113%)

Transjamaican Highway (+113%), a concessionaire and operator of two toll roads in Jamaica, was another big winner. They were also on my radar during the year and in fact, selected them as the best listed toll road opportunity I had come across in markets (7x P/E, 65% EBIT margins with 10-15% operating profits CAGR potential).

My worries about the long-term political threat to toll roads’ pricing power proved irrelevant in this situation, and growth remained strong, particularly in the May Pen and Spanish Town Toll Plazas.

Since going public 6 years ago, Transjamaican Highways has now been a 6-bagger, or 9-bagger with dividends reinvested.

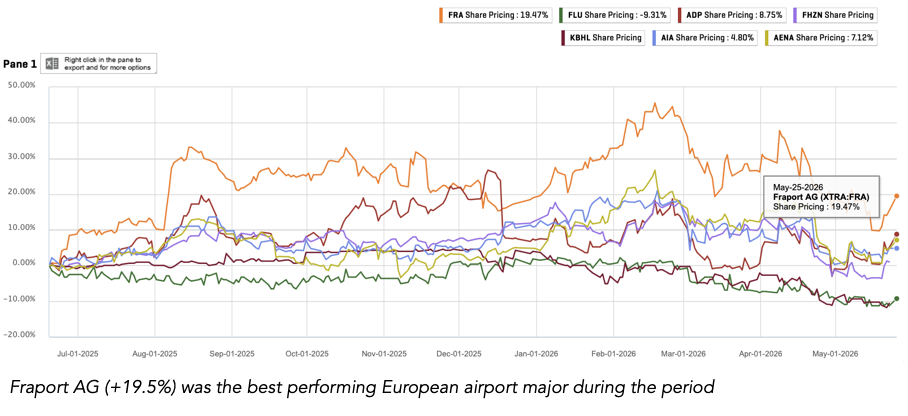

Fraport AG (+20%) - The reader’s recommendation

A couple of readers brought to my attention that I had ignored Fraport’s turnaround opportunity when I first published the deep dives. They were right.

Fraport (+20%) was the best performer among the 7 major European airport stocks, beating my own European recommendations, Aena (+7%) and Athens International Airport (+5%).

Unlike the emerging markets companies discussed earlier, I haven’t followed Fraport as closely and will spend the next few weeks closely analysing its fundamentals.

Betting on transport infrastructure

There were multiple other winners around the world, and the year proved once again that transport infrastructure remains an industry that an investor with a global equities and quality focus should follow closely, given the breadth of investment opportunities available.

From an allocation standpoint and as I’ve spent more time learning the ins and outs of the industry, I’ve increased my maximum portfolio weighting from 15% to 20%. I also remain optimistic about the companies we deep dived last year (OMA, ASUR, ICTSI) and plan on updating their investment cases to premium readers in the coming weeks.

Current Middle East tensions have also improved the valuation entry points to new potential names, and I have included Aena in the core portfolio watchlist. Should valuations further drop, you can expect an extensive deep dive in the coming months.

Dede, in your initial review of transport infrastructure companies, I did not see Promotora y Operadora de Infraestructura (PINFRA.MX) listed. At the time I figured it was not interesting to you. But it has performed quite well (the underlying business and the stock) and is still not expensive. So I am curious why it was excluded. Not that any of us will catch everything, just wondering if there was anything I missed or am missing now.

Why are you still optimistic on Aena and Athens international Airport. What do you foresee is likely to change in the global market dynamics to lead to a higher market return than in the last year. What upticks in their ecospace exist to warrant continued optimism!