FactSet Research Systems

Buying the dip

Yesterday, I increased the Fund’s FactSet position by 50%, bringing it to a position size of 7.5% of the Fund.

The reason for this was that at its current market cap of $8.26 billion, it breached our 20% IRR target (6% earnings, growth, exit multiple of 23x and a net effect of $3.3 billion in buybacks and dividends over the next 5 years).

Year to date, FactSet’s shares have declined by -23.3% and currently trade at 13.8x its trailing net profits (P/E ratio). For context:

Since going public in 1996 and also in the last 10 years, FactSet’s shares have averaged 31x P/E, meaning its current earnings multiples are less than half of its long-term average.

The lowest its P/E has ever reached is 13.3x during the depths of the financial crisis (20/11/2008), and we are now within 5% of its all-time low.

The market is apprehensive about the potential impact of AI, a theme we discussed extensively in the FactSet deep dive. This was particularly evident yesterday after the release of Anthropic’s plugins for Cowork supporting more specific roles such as legal, finance and data analysis.

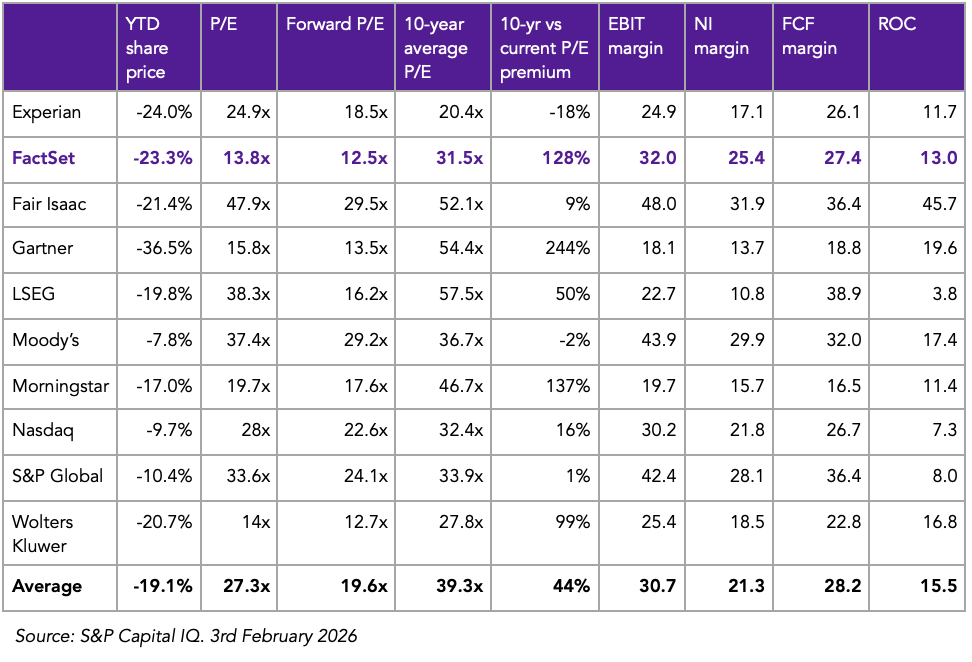

For further assessment on the state of markets in financial data services, I highlight 9 comparable companies in the table below, highlighting their share price performance year to date, earnings multiples and performance on four key profitability metrics.

As highlighted, the ten companies traded at relatively high multiples over the past 10 years, an average of 39x, a 44% premium to current multiples, led by Gartner (244% multiples premium), Morningstar (137% multiples premium) and FactSet (128% multiples premium).

It’s undoubtedly clear that Gartner (54x) or FactSet (31x) should never have been at such high multiples, but the more relevant question is, does the market undervalue their current worth?

While I won’t rehash the full AI threat (or opportunity) to FactSet, it’s important to highlight that Claude, like other LLM’s, does need inputs, and you can learn more about its current integration with FactSet here.

AI and LLMs like Claude will undoubtedly lead to some seat compression for FactSet’s clients. Still, they do make FactSet more usable to a broader market (investor relations teams, wealth advisors and areas of portfolio analytics).

As I modelled in the initial FactSet valuation, I suspect we’ll see more user growth (6.4% 5-year CAGR) in the long term, but at slightly lower revenue per user (-0.12% 5-year CAGR, $9,723 per user by 2030 FY). Further evidence of this was the Barclays and FactSet multiyear agreement announced last week, where FactSet will provide Barclays with access to its products data and other solutions.

Second, from my research speaking with existing (and past) FactSet users, it was clear that many were aware of the growing list of alternatives to FactSet. Still, when asked if they’d cancel FactSet tomorrow, there was an overwhelming no due to three reasons: trust built over decades, near-guaranteed accuracy and its growing range of proprietary data.

Thirdly, an important point to note with financial services is that FactSet’s core customers, investment banks, private equity firms, and sell-side analysts, among others, are in constant competition with one another. Their goal isn’t to have the lowest cost base of data, but rather, to have the deepest access to data and efficiently. It’s why Goldman Sachs analysts continue to work 80+ hour weeks, nearly 100 years after John Maynard Keynes predicted 15-hour working weeks as the norm.

I can’t imagine a world where Goldman Sachs cancels its FactSet subscriptions, knowing fully well that nearby competitors for deals like JP Morgan and Morgan Stanley continue to access FactSet’s growing breadth of banker efficiency solutions.

Portfolio allocation (see updated model below)