Latour AB 2.0

A valuation update

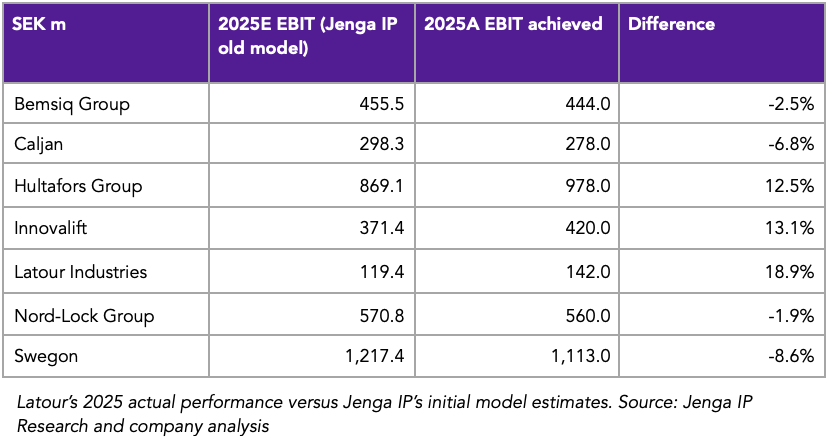

Last week, I initiated (but now sold) a 5% position in Latour after it met my initial 15% IRR hurdle based on earnings estimates from my 2025 valuation model. However, I spent the past week poring through Latour’s filings and those of its 10 listed investments and concluded my initial assumptions from last year were too optimistic, and have now updated my Latour valuation model.

Based on the updated valuation, which I will walk you through in this report, I estimate that Latour’s shares offer an IRR of 11.3% to 2030. Given this is below my 15% hurdle rate for new investments, I sold my investment in Latour’s shares for a small 0.2% gain. Latour remains on my core portfolio shortlist, and after discussing its valuation, I will discuss what price would make me reenter its shares.

A Latour reintroduction

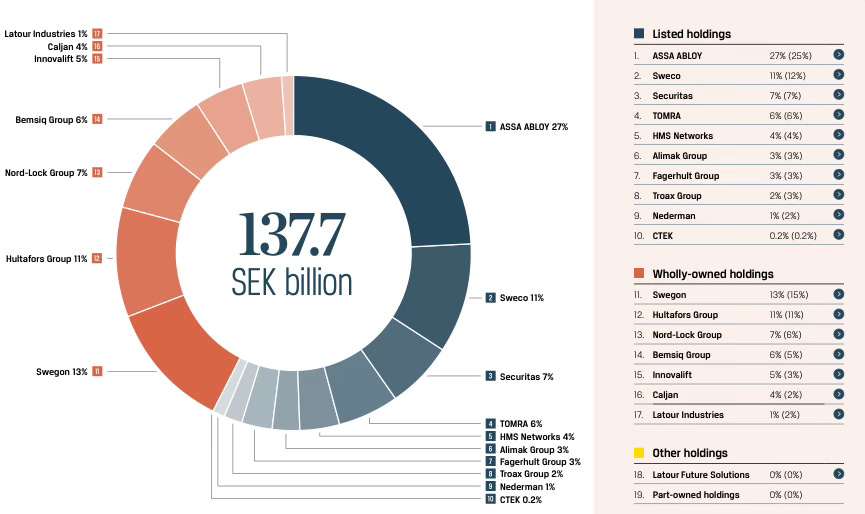

Latour is a Swedish industrial conglomerate, part family office and part serial acquirer. You can read my extended deep dive here or a summarised version here. Its business model is split between its wholly-owned operations (7 companies) and its listed investment portfolio (10 companies). Let me first discuss the wholly-owned operations.

On average, Latour aims to achieve 10% revenue growth with 15% operating margins and return on operating capital over the economic cycle.

1. Wholly-owned operations

Latour fully owns 7 industrial companies. At their core, these diversified companies serve industrial niches, providing mission-critical tools and services to customers in the building and construction (Bemsiq, Innovalift, Nord-Lock, Swegon), warehousing (Caljan) and tradespeople (Hultafors) industries.

Although diversified and mission-critical, like most industrial companies, their earnings growth is still somewhat subject to the European and global industrial cycle. For example, if there’s a slowdown in building and industrial activity, tradespeople are left with lower work activity and incomes and are less likely to spend EUR 110 replacing their Snickers workwear trousers. Despite being critical for buildings, Swegon’s HVAC solutions demand will decrease if its residential property customers anticipate a real estate market slowdown.

Among these 7 companies, Swegon, a manufacturer of HVAC solutions, is the largest, representing 13% of Latour’s NAV or 28% of the wholly-owned division. Bemsiq (6% of Latour’s NAV), a serial acquirer in building automation and metering, has been the fastest grower of the 7 companies in recent years (22% EBIT 5-year EBIT CAGR), mainly driven by Latour’s aggressive acquisitions of smaller companies like Eelectron and QEL in the KNX home automation industry.

Finally, Nord-Lock, in the bolts and fasteners industry, is the most profitable of the 7 wholly-owned companies, often earning EBIT margins of ~25% and a return on operating capital of ~30%.

I will next walk you through their valuations.

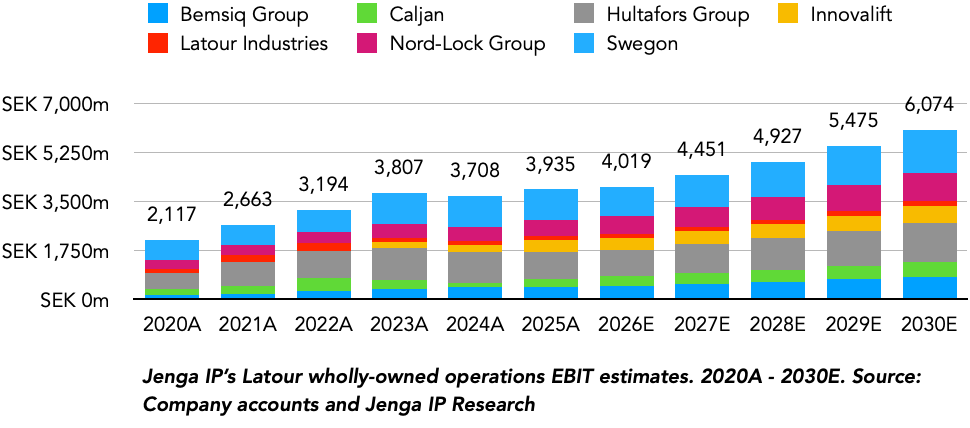

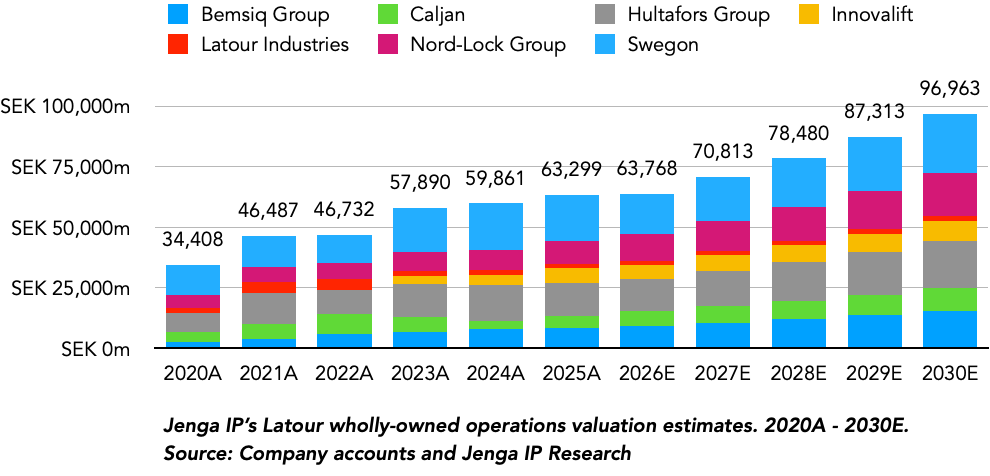

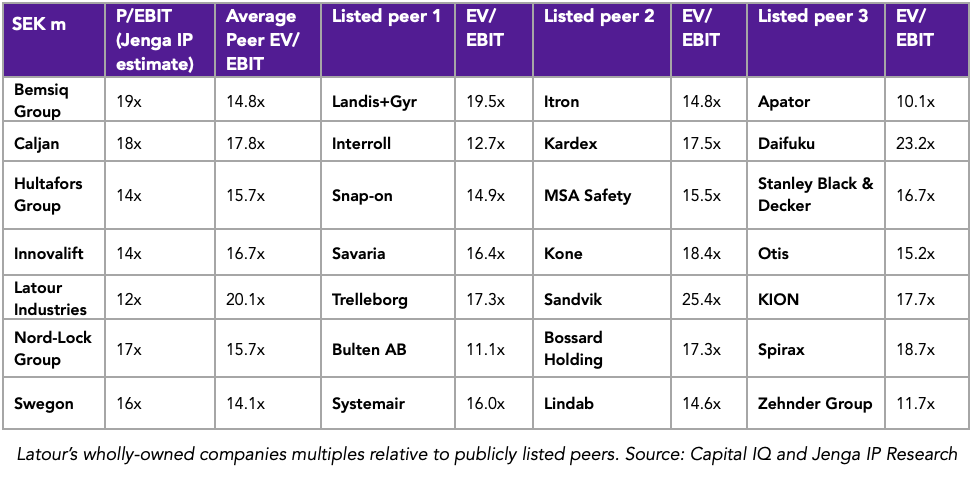

Latour wholly-owned operations valuation

Despite being private companies, my valuation approach is still the same as with public companies. That is, estimating where earnings could grow to in a conservative base case scenario and concluding on an earnings multiple that best reflects its business quality (resilience, profitability, pricing power, etc.) and growth prospects. As a reality check tool, I also assess the earnings multiples of listed per group companies.

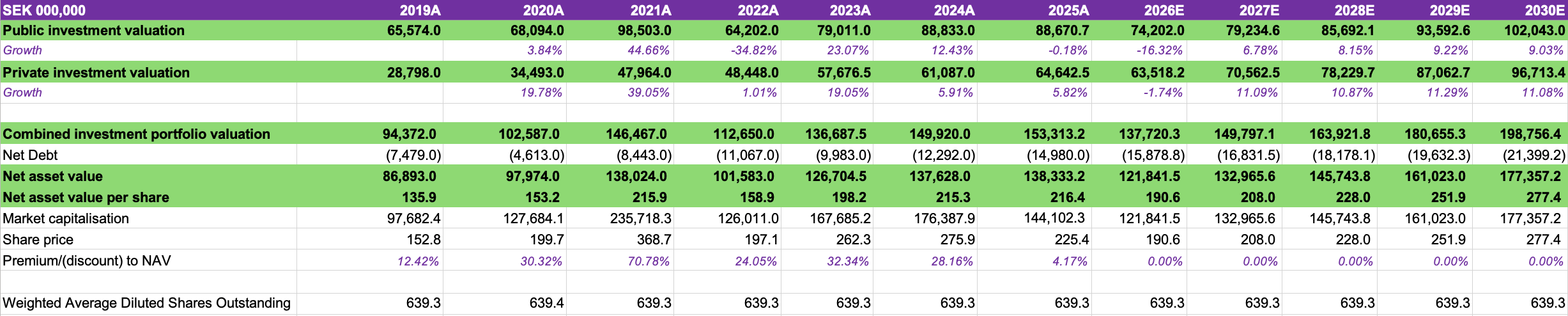

The table below summarises how I view Latour’s wholly-owned operations EBIT multiple, current valuation and earnings growth over the next five years and 2030 exit valuation.

The first two columns highlight how Latour values its holdings, which is on a price-to-EBIT multiple basis. Using this same approach, I revised my own exit multiple, which, on average, is just slightly less optimistic than Latour’s management, explaining why my valuation of its wholly-owned portfolio is roughly 2% lower or SEK 1.34 billion as at 2025 year-end (management’s SEK 64.6 billion versus Jenga IP SEK 63.3 billion).

Compared to management, I’m slightly less optimistic on Innovalift, Swegon and Latour Industries earnings growth and business quality prospects, which explains their lower exit multiple when compared to the median management range. For example, management values Innovalift at 16x EBIT while we value them at 14x EBIT.

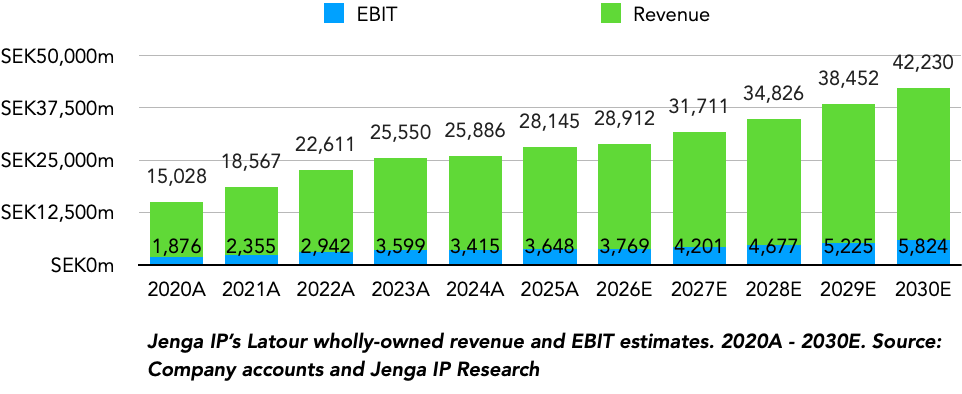

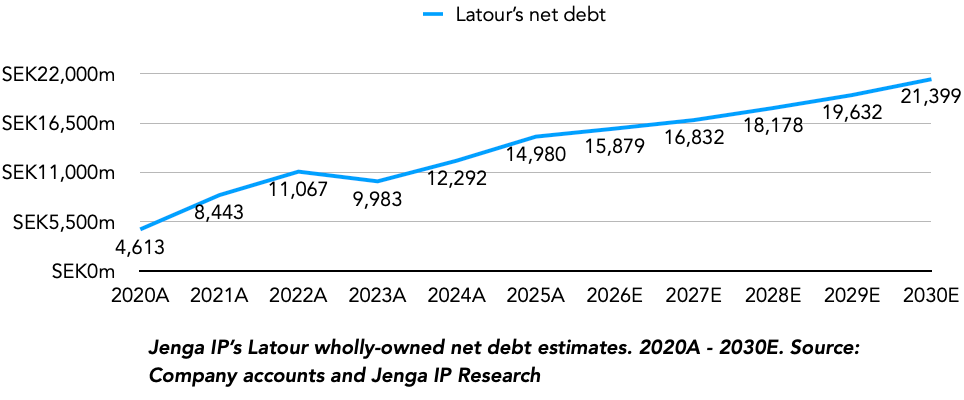

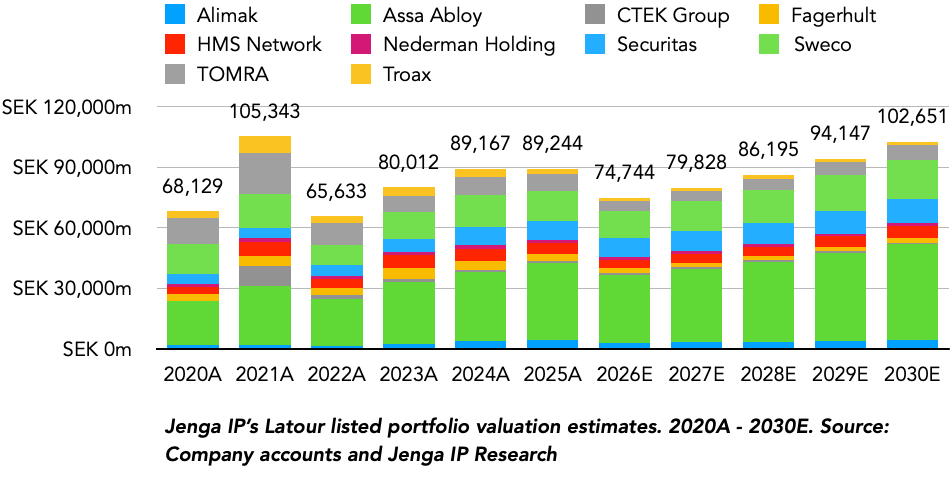

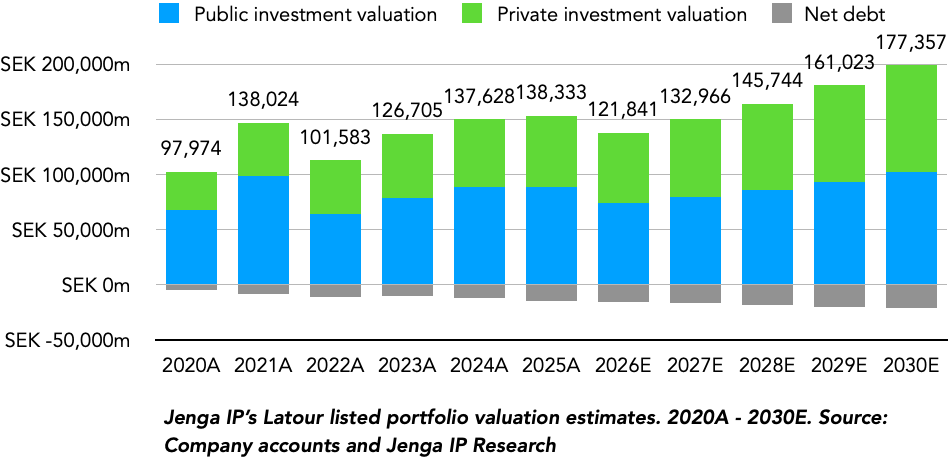

The 2020 to 2025 five-year period was exceptionally impressive for Latour, with revenue and operating earnings growing by 13.3% and 14.2%, respectively, above its 10% annual growth target. It might be tempting to project that growth for the next five years, but the aggressive growth during this period came at the expense of balance sheet strength, with net debt more than tripling during the period (see chart below).

Given how aggressively Latour put its raised debt to work through acquisitions across its subsidiaries, it will be far more difficult to repeat such growth rates without exceeding its debt capacity limits. As a result, I expect acquisitions to play a lesser but important role for Latour over the next five years.

Finally, two of these seven companies, Innovalift and Bemsiq, were created during the period, and it’s typical for Latour to supercharge new spinouts during their first years. Bemsiq, for example, tripled its revenue and operating capital between 2020 and 2025.

It’s possible Latour could spin out or create a new platform company over the next five years, but to be conservative, I don’t include this in my analysis and view it as an added optionality to its investment case. To further assess how I concluded on these growth estimates, let’s briefly discuss their overarching themes.

Bemsiq and Innovalift - Aggressive acquisitions

As Latour’s newer companies, Bemsiq and Innovalift, have been more aggressive on the acquisition front and plan to maintain the pace with explicit goals of doubling 2024/2025 revenue by 2029. Although my own growth estimates are below management targets, between both companies, I believe Bemsiq has a higher chance of achieving this. Compared to Innovalift’s elevator services industry, Bemsiq’s metering and building automation offers more industry growth drivers and acquisition targets, given its less oligopolistic market structure.

From a profitability and return on operating capital lens, Bemsiq’s business also requires less capital, and will also contribute to its performance during the current currency headwind, tariffs, and broader geopolitical environment. Innovalift’s Turkey exposure through Arkel (est. at 19% of revenue) could add to near term challenges for Innovalift. That said, 40% of Innovalift’s revenue are from the more recurring components and maintenance division and I expect the division to standout.

Hultafors Group, Swegon and Nord-Lock - Latour’s stalwarts

Latour has held each of these three companies for over 20 years, and combined, they represent roughly two-thirds of Latour’s wholly-owned companies. Despite their maturity, revenue and earnings growth have remained impressive, with both compounding by 10-13% over the past five years, ahead of most publicly listed peers.

While it is tempting to simply project this growth for the future, I suspect Hultafors and Swegon will likely have a more difficult acquisition market while operating conditions could become more competitive. Swegon’s HVAC portfolio is more tilted to residential and office customers than growth markets like data centres, limiting its ability to capture mid-term growth trends.

For Hultafors, although PPE remains a significant share of revenue (69%), the hardware hand tools, particularly in North America, face a more difficult construction market, coupled with more pressure from lower-priced retailers Husky (Home Depot), Kobalt (Lowe’s) and Hyper Tough (Walmart).

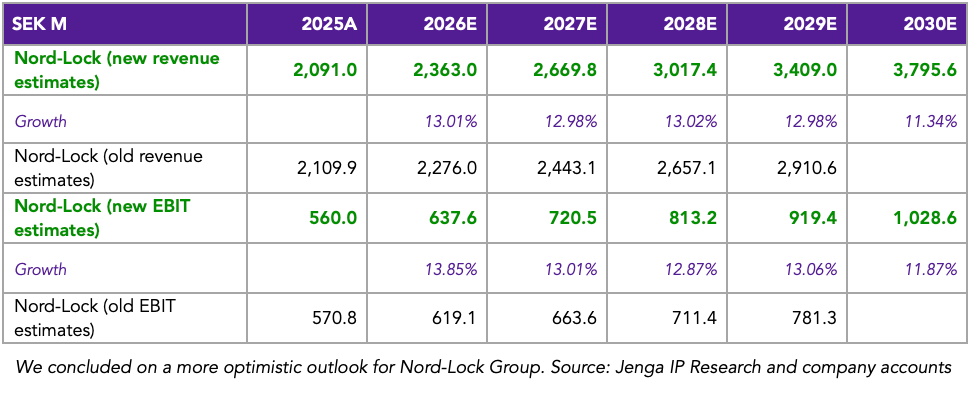

From the table below, you might notice my increased bullishness for Nord-Lock’s revenue and operating earnings.

The more I study the fastener and precision-machined components market, the more I appreciate its attractive combination of consolidation opportunities, pricing power and exposure to structurally growing end markets. A recent example is Nord-Lock’s acquisition of the UK-based Energy Bolting, a manufacturer of specialist fasteners mainly catering to the oil and gas, power generation and marine industries.

Although its UK Companies House filings don’t reveal its income statements, its balance sheet is strong, and there are hundreds of companies worldwide that could fit into Nord-Lock’s portfolio.

“In 2025, sales exceeded SEK 2 billion, with profitability remaining strong. The ambition is to double revenue by 2028. This will be achieved through a combination of organic growth and selective acquisitions.” - Daniel Westberg, CEO of Nord-Lock Group

Caljan - Cyclical turnaround

As I had suspected last year, I expected 2025 to be a turnaround year after two years of declining sales and operating earnings, with the momentum continuing in Q1 2026. Caljan’s telescopic conveyors are quite lumpy in sales and dictated by e-commerce market cycles. During boom times, customers like DHL and Amazon are more likely to invest in additional conveyors, while during downtimes, there’s typically little demand for new machinery.

For the long term, I don’t see much growth for Caljan, and I expect them to surpass their 2022 peak earnings sometime between 2028 and 2030.

Listed peer valuations

As a reality check on my valuations, I assessed listed peers, and the table below compares my valuation multiple to three listed peers for each Latour wholly-owned company. On average, my valuations are broadly in line with markets, which provides additional comfort that our estimates are conservative.

2. Latour’s listed portfolio

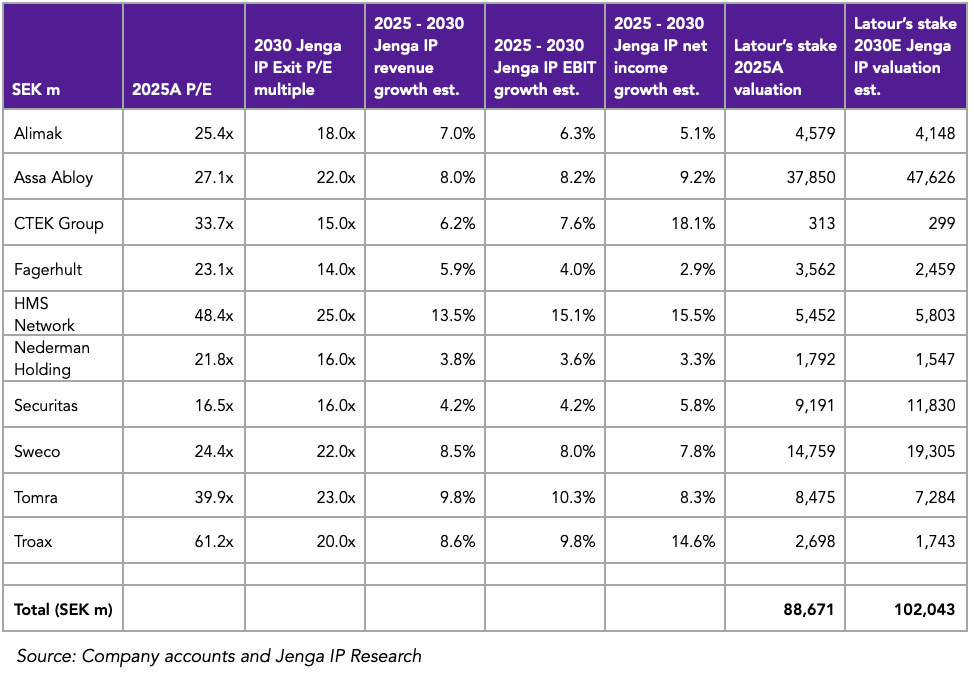

Rather than simply taking the current market cap of Latour’s 10 listed investments as the intrinsic valuation, I assessed these companies assuming we are making long-term investments in them, forming estimates of their 5-year revenue, EBIT and net income growth, and then concluding on P/E multiples that best reflect their business quality and growth characteristics.

While my individual analysis isn’t as deep as single company deep dives, I spent some time poring through filings, capital markets day transcripts, quarterly presentations, sell-side reports and broader materials on each of the companies to conclude on these figures.

The table above maps out my overall analysis of the ten listed companies, highlighting:

Current 2025 end-of-year P/E

My 2030 exit multiple

2025 - 2030 revenue, EBIT and net income CAGR estimates

Current valuation of Latour’s stake

2030 Valuation of Latour’s stake based on the exit multiple and net income estimate

As concluded from the table, I expect Latour’s publicly listed portfolio to deliver a 5-year annualised return excluding dividends of just 2.9% (SEK 88.7 billion to SEK 102 billion by 2030), and three problems contribute to my lower return estimate:

Assa Abloy and Securitas growth challenges

HMS Network and TOMRA - Expensive valuation

Sweco - A more challenging AI reality

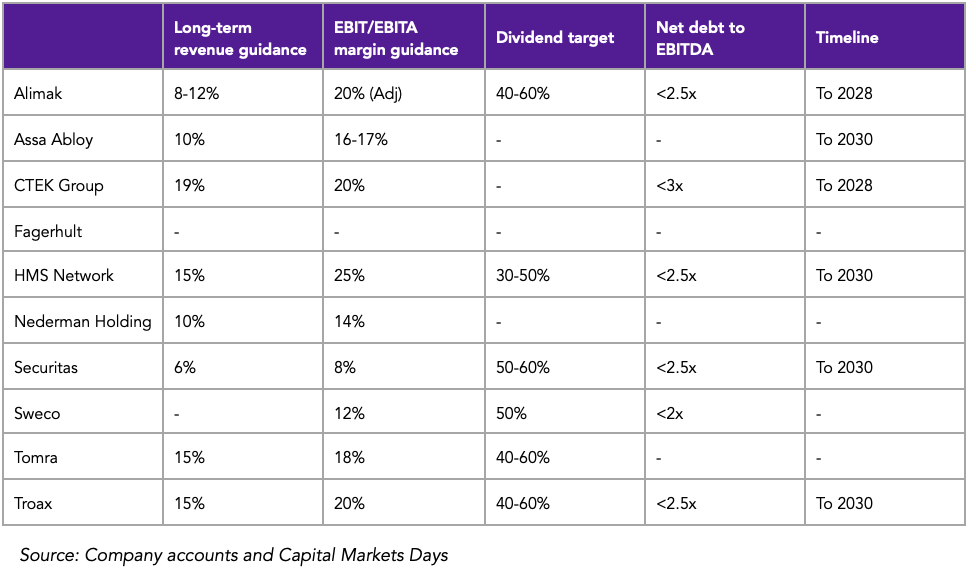

Before discussing these three issues, I want to highlight management’s own guidance from their Capital Markets Days.

Excluding HMS Network’s 15% revenue growth target and possibly Assa Abloy’s 10% revenue growth target, I suspect it will be challenging for the rest to meet these management revenue targets over the mid-term.

On a margin basis, the management targets appear more achievable. Although my estimates differ slightly (see valuation model), they are roughly in line with my own margin estimates during the period.

Assa Abloy and Securitas - Growth challenges

Both companies are Latour’s largest (Assa Abloy - 27%) and 5th largest (Securitas - 7%) holdings, and combined, represent a third of Latour and, as such, their outcomes severely impact Latour. Historically, both companies have done fairly well, but as they’ve gotten larger, it’s harder for Assa Abloy’s acquisitions to drive incremental growth while Securitas’s larger scale poses threats to labour costs and global wage inflation.

To date, Assa Abloy has made just around 400 acquisitions and a decade ago, they could probably achieve their 5% annual acquisition growth with just 10 companies, but today, it needs 25-30 acquisitions to meet the same target. In Q1 2026, Assa Abloy completed just 3 acquisitions, representing 0.4% of its 2025 revenue.

Encouragingly, both companies are managing their costs well and have so far dealt with tariff challenges well, with Assa Abloy raising prices across its products.

HMS Network and Tomra - Expensive valuation

If valuations didn’t matter, both HMS Network and TOMRA, two fairly profitable, acquisitive, and organically growing companies, could have joined our portfolio individually. The challenge, though, is that valuations do matter, and at the start of the year, they were valued by markets at 48x and 40x their respective net profits.

At such high valuations, both companies would have to grow profits north of +25% CAGR to justify such valuations while making an attractive IRR. The cost of this high starting valuation is already affecting Latour with Tomra’s shares declining -38% YTD after announcing a Q1 2026 profit warning.

Sweco - A more challenging AI reality

I marginally reduced my exit multiple from 23x to 22x for the Swedish architecture and engineering consultancy due to AI. While AI doesn’t replace architects, as I study how companies are implementing AI, I see a world where, rather than requesting 20 billable hours, Sweco’s customers could build initial drafts with AI and then request 15 billable hours, thus reducing total hours required.

Compared to more traditional technology or management consultancies, Sweco is certainly more insulated from this risk, but not fully immune. I suspect this risk partially contributed to the slowed sales experienced in Q1 2026, and I have revised my revenue and net income estimates. To combat this risk, though, I take comfort in Sweco’s above-inflation revenue per employee across its 8 regions, particularly in the UK, Germany and Central Europe.

At current market prices, Sweco still offers the most attractive IRR among the Latour listed investments and I have upgraded them to my core shortlist.

Latour’s valuation

Based on the wholly-owned and listed investments analysis, I arrived at a Latour valuation model by mapping out the net debt (see grey bar above) and annual dividend payments, which is guided by its target of paying 100% of dividends received from listed companies and 50% from private companies out to shareholders.

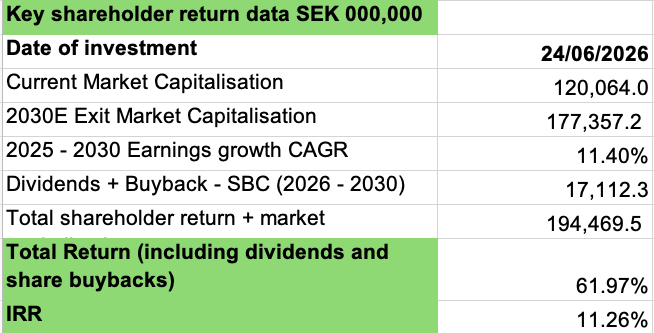

Overall, this leads to a 2030 estimated NAV of SEK 177.4 billion or SEK 277 per share.

Based on current valuations, this leads to an IRR of 11.26%, above 9% for an undervalued status but below the 15% IRR target for new investments which led to my sale.

Should Latour’s shares decline to SEK 161 per share, I’m happy to reenter its shares. But for now, Latour stays on the core watchlist.